2019 Precision Agriculture Dealership Survey: More Moves Toward Decision Agriculture

July 21, 2019

July 21, 2019 Editor’s note: The CropLife® magazine/Purdue University Precision Agriculture Dealership Survey is the longest-running continuous survey of precision farming adoption. The 165 respondents included cooperatives (16%), independent retailers (37%), and retailers that are part of a regional or national chain (47%).

View all

The 2019 Precision Agriculture Dealership survey shows further steps toward a future in which crop management decisions will be increasingly guided by data collected from farmer-customer fields. Sensing-technology services, such as grid/zone soil sampling, satellite and unmanned aerial vehicle (UAV) imaging, and yield mapping, all showed steps up compared to the 2017 results. Corresponding were increases in all variable-rate services — for fertilizers, lime, prescriptions for variable-rate seeding, and even for pesticides, although that remains relatively small.

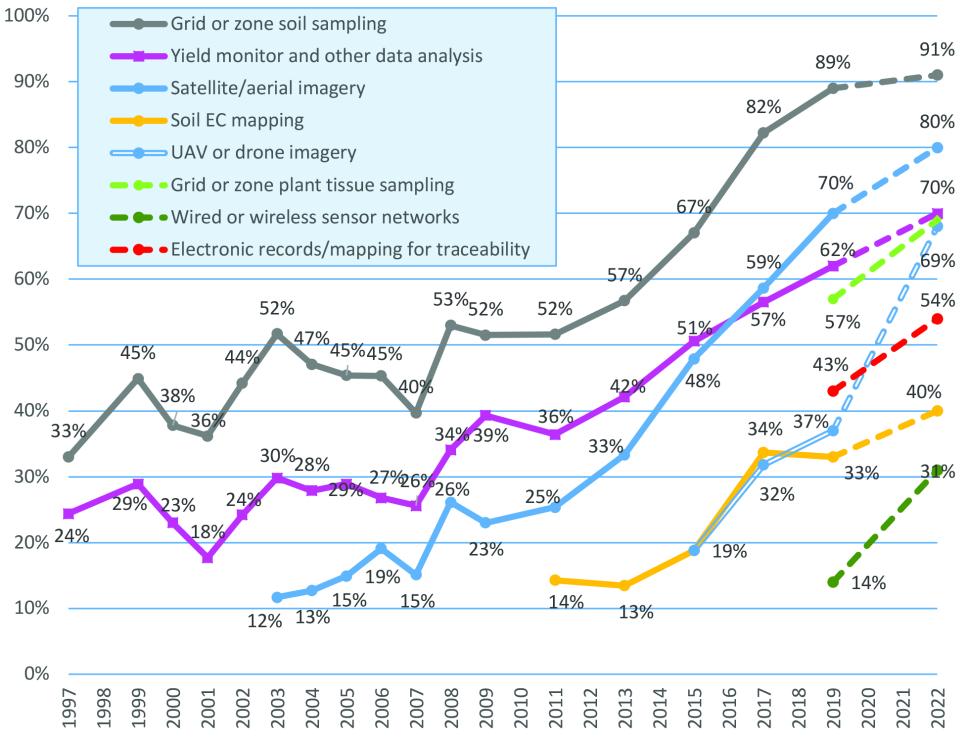

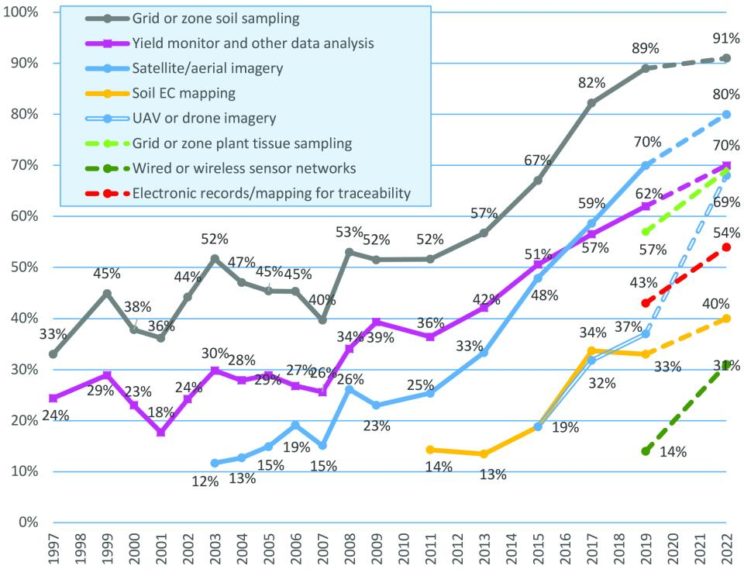

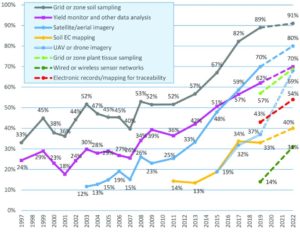

After longer than a decade in which only around half of the dealers were offering grid and zone soil sampling, this increased to 67% of dealers offering in 2015 to 82% in 2017 and now at 89% (see Figure 1 in slideshow above). Dealers offering satellite imagery — a possible foundation for creating management zones or guiding site-specific decisions — increased from 48% in 2015 to 59% in 2017 and 70% now. Similar increases were seen for dealers offering UAV services to customers and for dealers offering yield monitor analysis services.

Added to the survey this year were questions about dealers offering grid or zone tissue sampling, at 57%, and electronic records/field maps, at 43%. It should be noted that the data represents the percentage of dealers offering these services, not the percentage of acres in which these services were applied. The 2022 results are what dealers anticipate they will offer in three years. Among dealers who do not currently offer, the largest increases identified will be in UAV/drone imagery and precision plant tissue sampling.

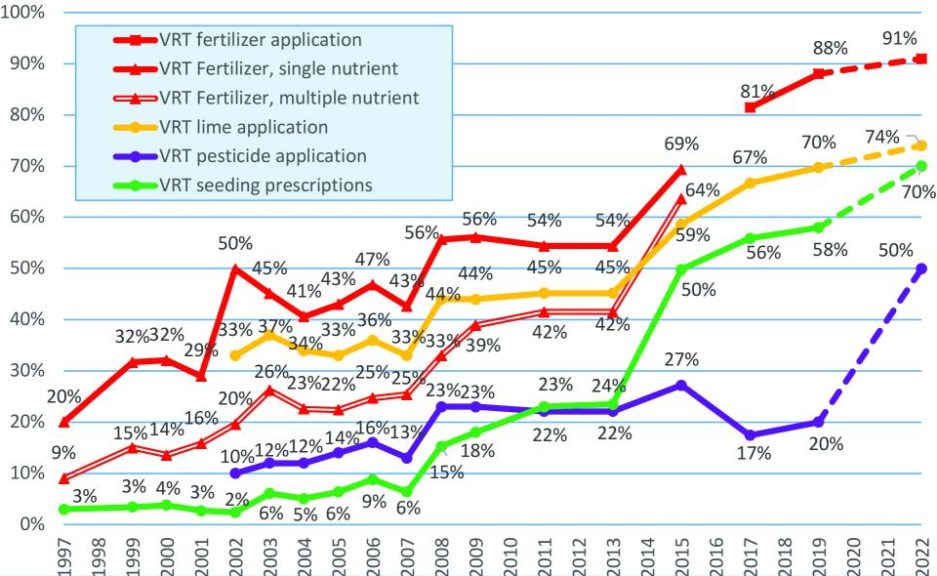

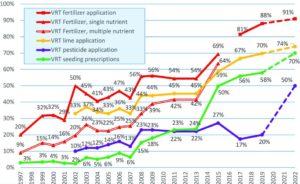

Variable-rate technology (VRT), where an informed approach is used to address variability across fields, has correspondingly increased (Figure 2). About half of the dealers for a decade were offering VRT fertilizer applications, but this increased to 69% in 2015 and 81% in 2017 and now is at 88%. VRT seeding recommendations have made a huge jump in the last few years, from 24% in 2013 to 50% in 2015, 56% in 2017, and 58% of dealers now offering these services. This dramatic increase in variable-rate seeding recommendations likely follows changes in planter technology that enable this and also the explosion in data service providers, many of these part of agricultural retail companies. Only 20% of dealers indicate they now offer variable-rate pesticide applications, but half of the dealers foresee they will be offering this in the near future — probably linked to new machine-vision technology that enables weed recognition and the targeting of individual weeds.

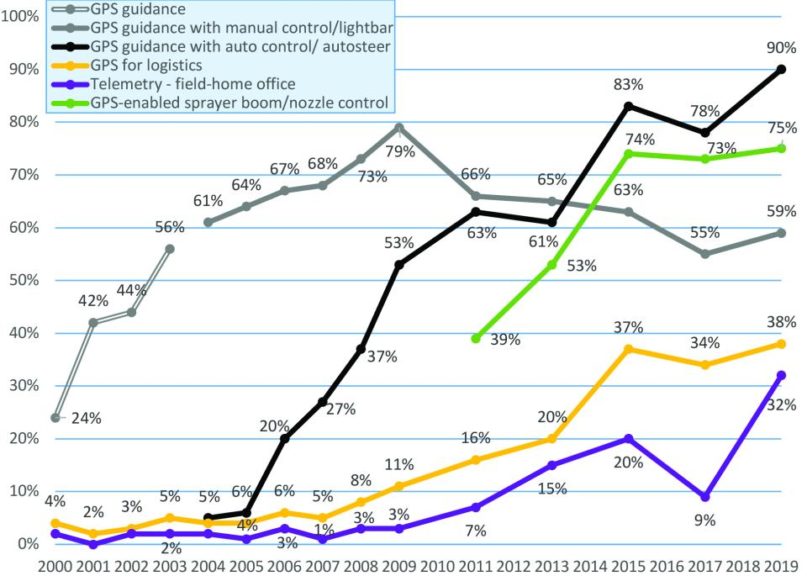

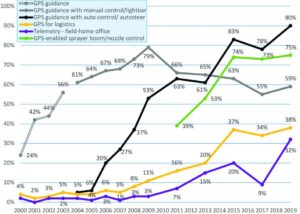

In contrast to the data-intense technologies that underlie decision agriculture is a set of automated practices that does not depend on a field’s agronomic characteristics, only a field’s size and shape and where the machine has been. The economic benefits of reducing overlaps and skips, allowing drivers to work longer hours with less fatigue, and to work through dust, fog, and through the night, have proven substantial for farmers as well as dealers. The use of guidance technologies by dealers for their custom pesticide and fertilizer applications indicate a maturing market, with 90% of dealers using autoguidance along with GPS-guided boom section/nozzle controllers on sprayers being used at three-fourths of the dealerships (Figure 3). Another guidance-related technology, sprayer turn compensation, is emerging with 24% adoption by dealers but only up slightly compared to 2017. Turn compensation adds value more subtly by helping to reduce over- and under-application rates vs. reducing doubling-up and skips. There are more dealers using telemetry to exchange information among applicators or to/from office locations and more dealers using GPS fleet management for vehicle logistics and tracking the locations of vehicles.

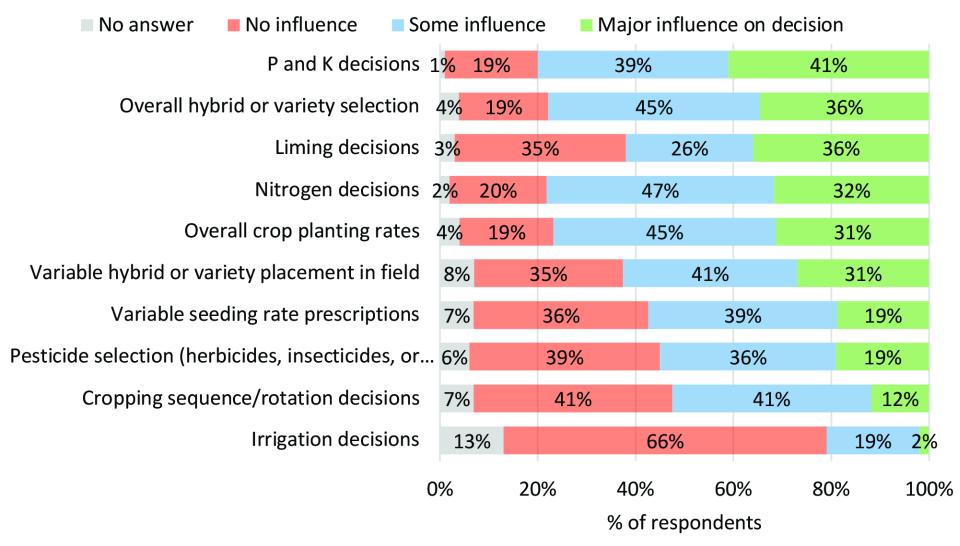

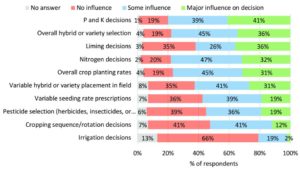

The biggest news for 2019? The impact of crop management decisions from pooled data. A new question in 2017 asked dealers to gauge the influence of data shared among farmers on a variety of factors related to crop management decisions (Figure 4). The 2019 survey showed a dramatic increase overall in the influence of pooled data — this would be data aggregated from multiple farms, either managed within the dealership or as part of an outside offering. For crop nutrient decisions, 80% of dealers said phosphorus and potassium decisions were at least somewhat influenced by pooled data, up from 43% just two years ago, and 79% saying nitrogen decisions were being influenced, up from 39% in 2017. Eighty percent of dealers (up from 39%) indicated pooled data had at least some influence for overall hybrid/variety placement, and 62% (30% in 2017) said it was influencing variable hybrid or variety placement in fields. Fifty-eight percent said pooled data was informing variable planting rate prescriptions, up from 30% in 2017. As mentioned before, some of this is likely driven by an increasing presence of data service providers. Less than half of dealers (47%) indicated their company had a customer data privacy statement and/or a data terms and conditions agreement similar to 2017.

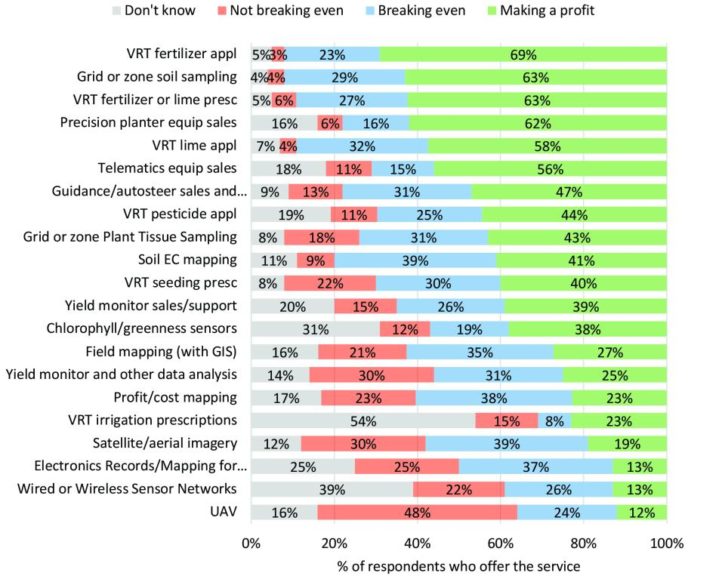

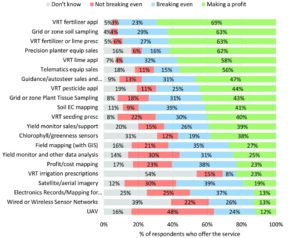

Finally, all of this technology in the end has to eventually pay its own way. This can be done in multiple ways — through increased returns for that specific activity but also through reducing the costs to the dealership, as might be the case with guidance, section controllers, or fleet logistics management for custom application services. The value could be indirect, such as enhancing customer relationships or providing a product or service not available from a competitor. When dealers were asked about profitability of the services they offer, precision soil sampling and VRT fertilizer applications stood out positively from the others (Figure 5), with over 90% of dealers indicating a profit or break even. Notable on the unprofitable side were dealers who offer UAV services, where 64% of those with a UAV indicated they were not breaking even or didn’t know, slightly more negative from two years prior, and for satellite/aerial imagery, where 42% were not breaking even or didn’t know — the same as two years ago.

Subscribe Today For