The 2025 CropLife 100 Report: The Definitive Fun With Numbers

For anyone paying attention to the agricultural industry these past 12 months, it should be painfully clear that one variable has dominated the news – numbers. Depending upon the source (or day), these numbers could look pretty rosy (more than $170 billion in net farmer income) to terribly bleak ($0 in U.S. soybean exports to China through the end of September).

Here at CropLife® Magazine, we love to play with numbers, too. For almost a decade now, our weekly videocast, CropLife Retail Week, has featured a segment at the end of each episode called “Fun with Numbers.” This offers co-hosts (and guests) the chance to see how well they’ve kept up with the myriad agricultural figures that appear each week across the worldwide web network of sources by selecting the correct answer from four choices.

In addition, for more than 40 years now, CropLife has annually polled the nation’s top ag retailers through its CropLife 100 survey to gauge the health of the entire industry. Naturally, numbers are a huge part of this effort.

View the 2025 CropLife 100 Rankings >>

So, with this introduction to the numbers question out of the way, what kind of numbers – both positive and negative – did the CropLife 100 ag retailers record in their computer spreadsheets in 2025? And more importantly, will any of these improve for the upcoming 2026 growing season, or do they indicate harder times ahead?

Let’s dive in and find out!

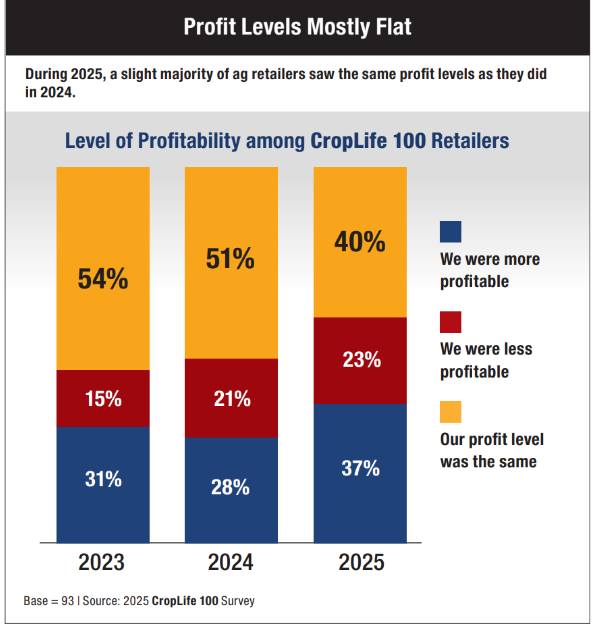

During 2025, a slight majority of ag retailers saw the same profit levels as they did in 2024. Source: 2025 CropLife 100 Survey.

Given how much uncertainty plagued the agricultural marketplace during the whole of 2025, the nation’s top ag retailers performed quite well during this year’s growing season – comparatively speaking. According to the 2025 CropLife 100 survey, the top ag retailers recorded overall revenues of $42.9 billion for the year. And while this did mark a downturn from the industry’s 2024 revenue ($43.3 billion), this 0.9% overall decline in sales wasn’t that significant.

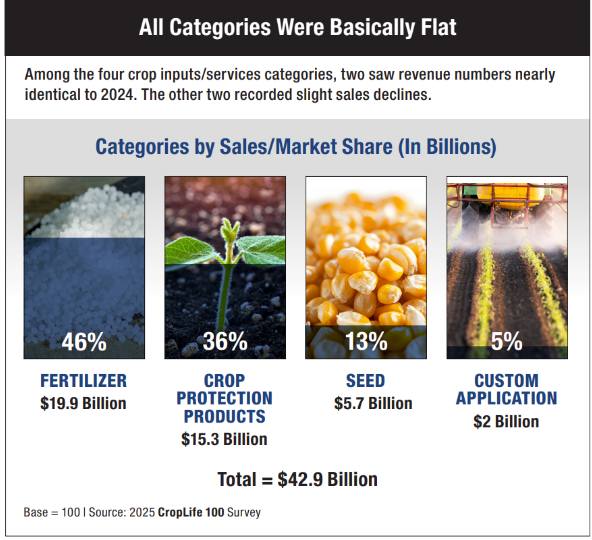

For the purposes of the CropLife 100 survey, CropLife asks the nation’s top ag retailers to share with us how the revenues did in four distinct categories – fertilizer, crop protection products, seed, and custom application (which includes ag technology, i.e., Smart Tech). These are presented here in descending order of their respective market shares compared with all the other categories. Normally, whenever the largest categories perform well, the overall market does as well.

And that’s what happened in 2025. According to the CropLife 100 survey data, both the fertilizer and crop protection products categories held their own during the 2025 growing season in terms of sales. In fact, sales in both categories were mirror images of the 2024 growing season figures.

Among the four crop inputs/services categories, two saw numbers nearly identical to 2024 for ag retailers. The other two recorded slight sales declines. Source: 2025 CropLife 100 Survey.

For fertilizer, 2025 sales topped $19.9 billion according to CropLife 100 ag retailers – identical to the figure the category managed for the marketplace during 2024. Likewise, crop protection product sales were similar – revenues for 2025 for this category hit $15.3 billion – the same figure achieved by the category during the 2024 growing season. Not surprisingly, both categories maintained their overall 2024 market shares of all crop inputs/services sales among top ag retailers in 2025, at 46% and 36% respectively.

For the third largest category of crop inputs/services – seed – the story of 2025 was a different and less positive. By the numbers, CropLife 100 ag retailers saw their seed sales during this past growing season decline slightly, falling 1.7% to $5.7 billion. Nonetheless, because this decline in sales wasn’t that large, the seed category still managed to maintain its overall market share among top ag retailers’ crop inputs/services at 13%.

Among the four categories, the hardest hit in 2025 was custom application. Here, according to the 2025 CropLife 100 survey, overall revenues declined $300 million, from $2.3 billion in 2024 to $2 billion this year – a 13% drop. Still, given how flat the rest of the marketplace was, the custom application category managed to hold its overall crop inputs/services market share steady at 5%.

The Sub-Segments Review

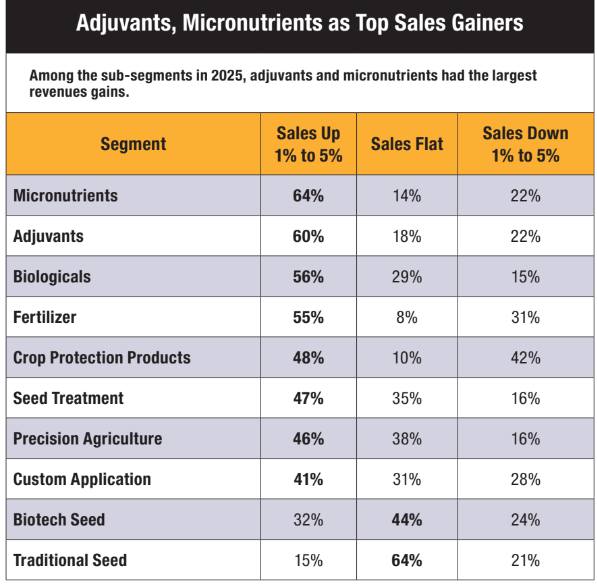

Besides the four major crop inputs/services categories, the annual CropLife 100 survey also tries to gauge how some of the sub-segments of the marketplace performed during the current calendar year. Here, as was the case with the four major categories, crop nutrition and crop protection products led the way in terms of sales performance.

Among the subsegments in 2025, adjuvants and micronutrients had the largest revenue gains for ag retailers. Source: 2025 CropLife 100 Survey.

For the 10 segments tracked in this portion of the CropLife 100 survey, respondents are asked to tell us how each performed during the current growing season in terms of revenues. There are three options: 1) Sales were up between 1% and more than 5%; 2) Sales were down between 1% and more than 5%; and 3) Sales were unchanged from the prior year. Any segment that scores better than 50% for sales increases is considered a success for the year. And in 2025, four of the 10 segments achieved this mark.

Leading the way was the micronutrients segment. Here, according to the 2025 CropLife 100 survey, 64% of respondents had sales increases of these products between 1% and more than 5%. Adjuvants weren’t far behind, with 60% of the nation’s top ag retailers seeing sales increases for these products during the year.

The other two segments to achieve more than 50% of their sales growing during 2025 were virtually tied. According to the 2025 CropLife 100 survey, 56% of ag retailers saw their biologicals sales grow between 1% and more than 5%. Meanwhile, 55% of respondents said their fertilizer revenues grew by the same percentages during the 2025 growing season.

Key Concerns for 2026

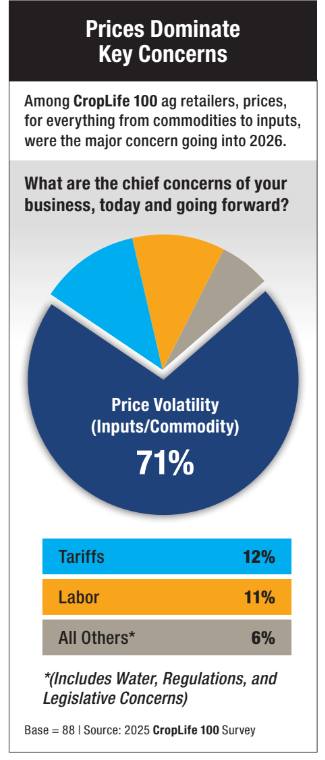

With the numbers for the 2025 growing season now in the books, it’s time to speculate on what kind of numbers the industry might see once the 2026 growing season gets underway. On this question, a big majority of the nation’s ag retailers are very, very troubled by all the negative numbers being brandied about for agriculture at the moment.

Among CropLife 100 ag retailers, prices, for everything from commodities to inputs, were the major concern going into 2026. Source: 2025 CropLife 100 survey

When asked about their chief concern about the agricultural industry going into 2026, almost three-fourths (71%) listed price volatility as the major issue. Given the answers from the 2025 CropLife 100 survey, this ranged from everything imaginable – from record low commodity prices for corn, soybeans, wheat, rice, and cotton to high crop input prices depressing retail sales to financial instability/accounts receivable issues at the farmgate.

Significantly, this represented a big jump in percentage for price volatility from the 2024 CropLife 100 survey. Last year, slightly over half of the nation’s top ag retailers (54%) listed price volatility as their major concern going into the 2025 growing season.

In second place among chief concerns was a new item – tariffs. By now, most in the agricultural marketplace are aware of how negatively trade tariffs have depressed U.S. agricultural export sales (with one-time major importer China purchasing no soybeans through the end of September 2025). Overall, 12% of respondents listed this as their chief concern going into next year’s growing season.

Finishing a close third behind tariffs was labor – as in finding/keeping good employees. For years, this issue was the No. 1 concern year in and year out for CropLife 100 ag retailers. However, it’s been overshadowed by other concerns over the past two years.

But to end this report on a high note of sorts, all of these concerns and flat revenue numbers for 2025 haven’t dampened the majority of ag retailers’ outlook for the 2026 growing season. When CropLife 100 ag retailers were asked on the 2025 survey to rank their level of confidence in the financial outlook for 2026 on a scale of one to 10 (one being low confidence, 10 being high), the majority (52%) believe that next year will rate between five and seven in terms of revenue. Another 27% think that next year’s growing season will rate between eight and 10. Only 21% think the 2026 growing season will be poor, rating between one and four.

View the 2025 CropLife 100 Rankings >>

Subscribe Today For