CropLife 100: No Changes in Sprayer Fleets for 2025

In the world of television, nobody likes repeats. However, in the equipment world, repeats of strong years are always welcome, especially when overall market economic conditions seem less than stellar.

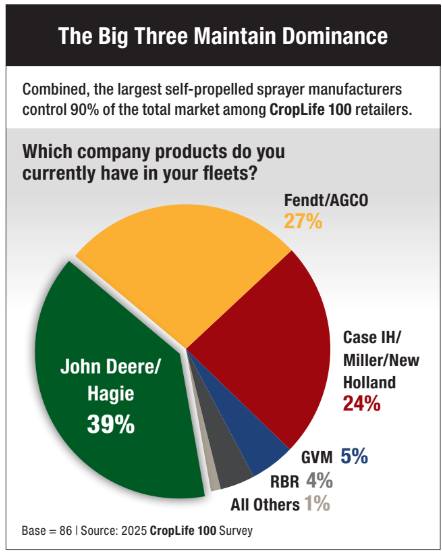

According to data collected from the 2025 CropLife 100 survey of the nation’s top ag retailers, the color mix in their self-propelled sprayers fleets remained remarkably consistent throughout the whole of the 2025 growing season. The Big Three equipment manufacturers – John Deere/Hagie, Fendt/AGCO, and Case IH/Miller/New Holland – continued their overall dominance among ag retailers, holding a combined 90% market share. Coincidentally, this was the same percentage these three industry giants held according to the data collected in the 2024 CropLife 100 survey.

Given these facts, it should come as no surprise that the individual market shares held by the Big Three among self-propelled sprayer fleets at the nation’s ag retailers remained static as well. According to the 2025 CropLife 100 survey, John Deere/Hagie had the largest share at 39%, followed by Fendt/AGCO at 27%, and Case IH/Miller/New Holland at 24%. This was identical to the market shares each of these companies held according to information from the 2024 CropLife 100 survey.

Furthermore, the remaining 10% of the market not controlled by the Big Three saw no appreciable moment either. According to the 2025 CropLife 100 survey, GVM and RBR Enterprise held 9% of this market share combined (split 5% to 4%, respectively). Again, this was identical to the market shares these companies had recorded among ag retailers during the 2024 growing season.

Still Buying Big Three

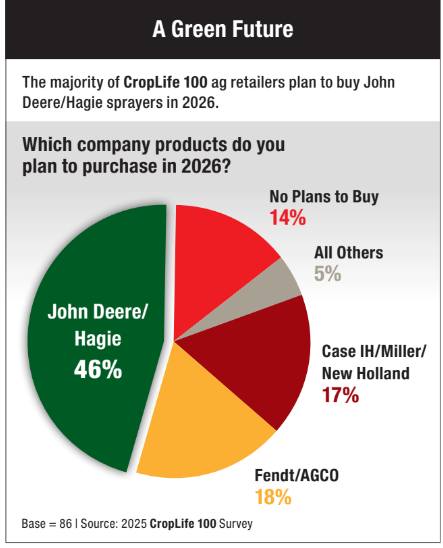

For market observers, the future of the self-propelled sprayers market going forward looks as if it won’t be markedly different in shape as it appears today. Overall, according to the 2025 CropLife 100 survey, 81% of the nation’s top ag retailers plan to continue buying their self-propelled sprayers for the 2026 growing season from the Big Three manufacturers.

Broken down according to the survey data, 46% plan to buy John Deere or Hagie sprayers next year, up slightly from 42% in the 2024 CropLife 100 survey. Purchases of Fendt/AGCO and Case IH/Miller/New Holland sprayers will be down slightly from 2024, with 18% of CropLife 100 ag retailers planning to buy Fendt/AGCO machines (vs. 19% in 2025) and 17% planning to purchase Case IH/Miller/New Holland units (compared with 18% in 2025). Another 5% plan to make their self-propelled sprayer purchases from some of the smaller companies in the marketplace, including GVM, RBR, and Horsch. The remaining 14% of the nation’s ag retailers have no plans to upgrade their self-propelled sprayer fleets for the 2026 growing season.

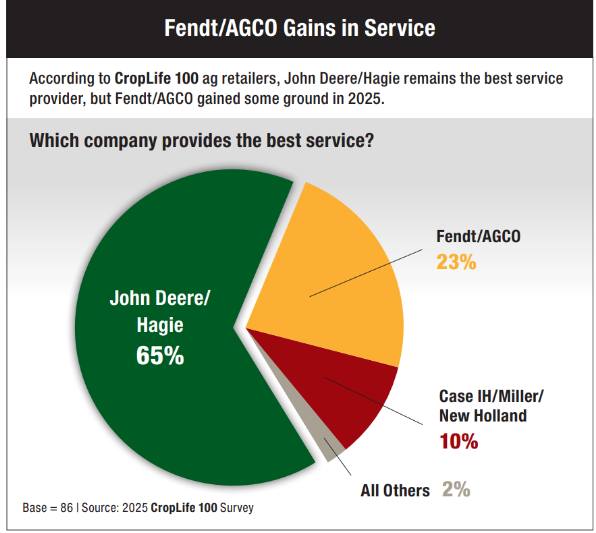

If there was one difference in the information collected in the 2025 CropLife 100 survey vs. the 2024 CropLife 100 survey when it came to equipment manufacturers, it was in the area of service. For several years now, the annual survey has asked the nation’s top ag retailers to rate which company they believe provides the best overall service to its customers. Each and every year, John Deere/Hagie has led the pack in this area, The company did so again in the 2024 survey, rated the best in service by 72% of respondents. Fendt/AGCO and Case IH/Miller/New Holland finished second and third, with 16% and

12%, respectively.

But according to the 2025 CropLife 100 survey, Fendt/AGCO has made a big move up in the service department among the nation’s top ag retailers. The Duluth, GA-based manufacturer of Rogators is now perceived as providing the best service to its customers by 23% of CropLife 100 ag retailers, an improvement of 7% vs. 2024.

Still, John Deere/Hagie leads among all self-propelled sprayer manufacturers when it comes to service according to 65% of CropLife 100 ag retailers. However, this is a decline of 7% from the 2024 survey data.

The remaining 12% of 2025 CropLife 100 respondents split their answers on the service question among Case IH/Miller/New Holland (10%, down 2% from the 2024 data) and “all others” at 2%.

Subscribe Today For