CropLife 100 Mid-Year Report: How Ag Retailers Are Dealing with Lots of Change

June 8, 2020

June 8, 2020 For agriculture, uncertainty is just a part of life. Numerous factors each year — such as weather and overall market economics — remain unpredictable, despite the best efforts of market watchers and expert analysts. Still, historically, most companies that earn their living from agriculture find these pundits normally “on the money” when it comes to their growing season forecasts.

Then, there’s what’s taken place the past two seasons, in 2019 and now in 2020. As most ag retailers and their grower-customers will attest to, economic outlooks for these two years haven’t been worth “a wooden nickel” in terms of their predictability.

And for the nation’s largest ag retailers, all this change in agriculture has been a serious challenge when it comes to maximizing their cash flows. However, most appear to be managing to make a buck or two despite all of this uncertainty.

Before looking at the present situation for the CropLife 100, a quick look back is in order. During our annual survey of the nation’s top ag retailers (published in December 2019), most ag retailers and their grower-customers had high hopes for 2020, financially speaking. When asked how their customers felt going into the upcoming season, the majority, 59%, believed 2020 would rank between a five and a seven in financial terms (on a scale of one to 10, with one being “poor” and 10 being “outstanding”). Another 23% thought that the 2020 growing season would rate between an eight and 10 in terms of growth potential, for a cumulative total of 82% thinking the year would rate a five or higher in profit terms. Only 18% believed that the 2020 growing season would rate a four or lower on the 10-count scale for profitability.

Of course, since the annual CropLife 100 report came out, the world has witnessed change at an unprecedented rate. Indeed, with the coronavirus pandemic gripping most of the globe, economic growth forecasts in many sectors have inevitability moved from positive to negative very rapidly. Given this climate, it would have been safe to assume agriculture might also experience some kind of negative change as well.

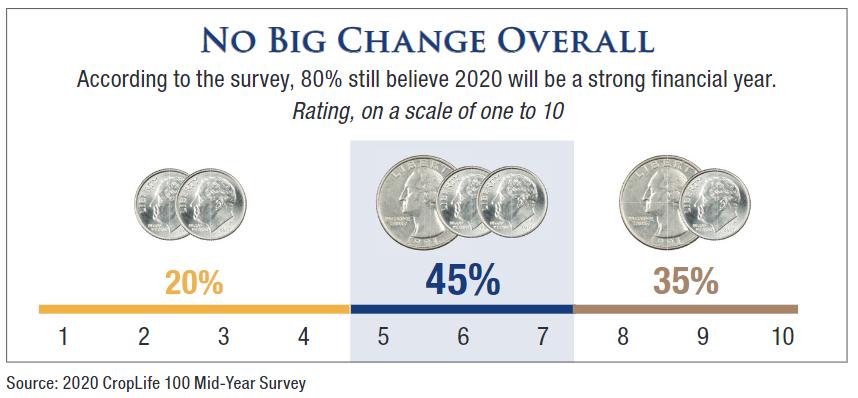

However, the numbers don’t support this . . . at least not yet. According to the 2020 CropLife 100 Mid-Year Survey, when respondents were asked to rate their financial outlook for the agricultural year at the midway point on a scale of one to 10 (one being worse, 10 being best), 80% still believe it will be better than a five. Broken down, 45% of respondents see the 2020 growing season has rating between a five and seven in terms of overall growth, down 14% from the 2019 CropLife 100 survey results. But 35% now rate 2020 as being an eight to a 10 in terms of growth, up 12% from the December findings. The percentage of ag retailers rating the 2020 growing season between one and four on the 10-point scale has risen only slightly, 2% to 20%.

The COVID-19 Factor

Perhaps a large part of this continued positive outlook for the 2020 growing season by the nation’s top ag retailers has to do with how the overall industry has weathered the COVID-19 outbreak. As the coronavirus pandemic continued to spread during the spring months, many cities and states issued “shelter-at-home” orders for residences, closed schools, and shut down many businesses such as restaurants and gyms to keep this new disease from infecting more individuals. Ultimately, this had a devastating effect on the nation’s economy, throwing millions of people out of work and causing numerous businesses to file for bankruptcy or close altogether.

Yet in the midst of all this economic uncertainty, ag retailers and their grower-customers continued to do their jobs, planting and working in the nation’s farm fields without serious issues. “Vendor supply, so far, is not an issue,” said John Oster of The Morral Companies, LLC, Morral, OH, during the spring planting season. “[We had a] minor hiccup on truck arrangement, but for now, we have no major issues.”

CropLife 100 ag retailer Asmus Farm Supply (AFS), Rake, IA, sent a similar message to its customers back on March 17. “AFS is having no supply issues with any of the crop inputs it provides customers,” said the note. “This includes seed, crop protection products, and plant nutrition items. We have enough on hand to satisfy our customer needs through the planting season.”

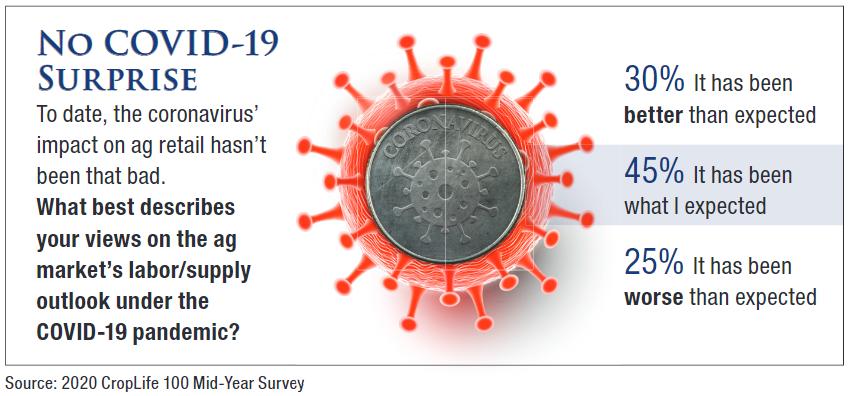

For the most part, the nation’s top ag retailers agreed with these views on COVID-19’s more minor impact on their bottom lines. In fact, when asked what effect the coronavirus has had on their businesses during 2020 thus far, 45% of CropLife 100 Mid-Year Survey respondents said it was “what they expected.” Another 30% said the economic fallout from COVID-19 was “better than expected.” Still, 25% of respondents the virus’ impact was “worse than expected” in financial terms.

The Inputs Report Card

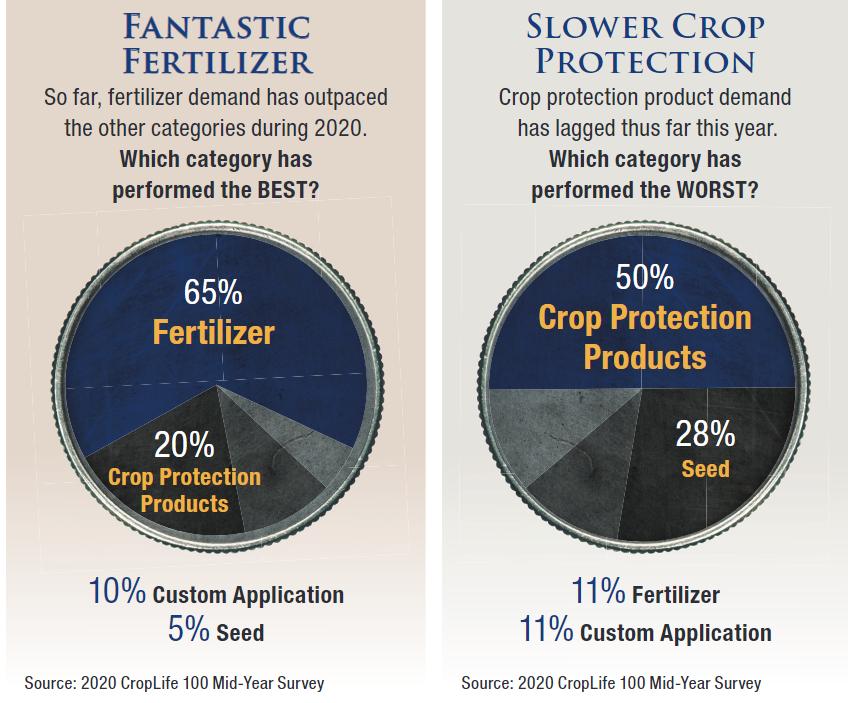

In terms of crop inputs and services, the nation’s top ag retailers definitely have a clear winner and loser thus far for the 2020 growing season. According to the majority of CropLife 100 survey respondents, fertilizer demand has been making the most sense (and cents) for them this year. In fact, 65% say this category has performed “better than expected” thus far this growing season.

As for why this seems to be the case, the answer seems to be two-fold. For one thing, the nation’s weather during the 2020 season has been rated “better than expected” by 55% of CropLife 100 ag retailers, according to the mid-year survey. During much of 2019, this wasn’t the case as the cool, rainy spring months spilled all the way into early June for many of the key Midwestern states. This kept fertilizer demand down for much of the entire 2019 growing season — from early spring into late fall, according to most experts.

The second reason for this apparent increase in fertilizer demand ties back to what’s being planted in the nation’s crop fields. During 2019, as the planting season stretched into early June, many growers shifted from planting corn to quicker growing soybeans. This likely depressed fertilizer demand as a result.

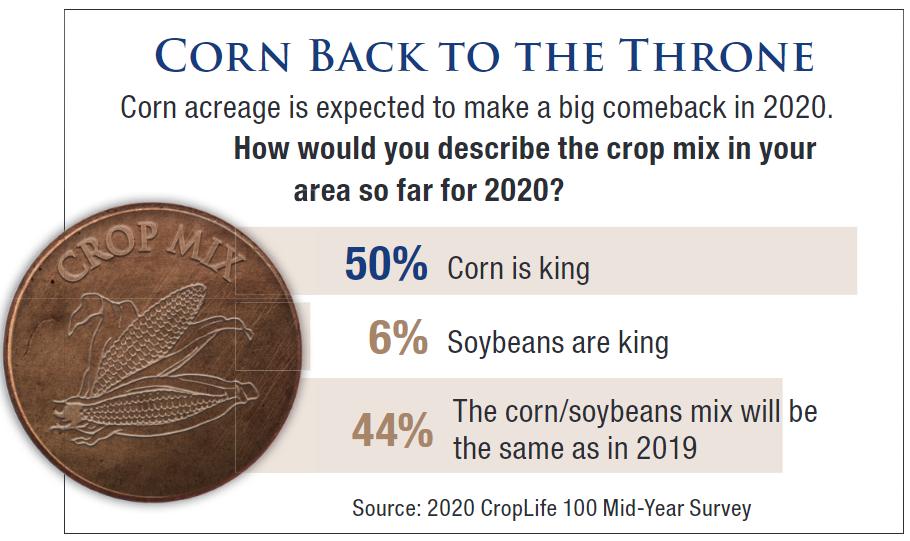

But in 2020, according to 2020 CropLife 100 Mid-Year Survey respondents, corn is making a comeback this year. Government statistics predicted U.S. growers would plant 97 million acres of corn in 2020, up 7 million acres from 2019 — and ag retailers agree. According to 50% of respondents, “corn is king” in 2020, creating a big demand for fertilizer to go into the nation’s crop field. Another 44% of ag retailers say the split between corn and soybean in their areas will be the “same as in 2019.”

As fertilizer fortunes have improved during 2020, two other crop input categories have performed a little less well. According to the survey, the crop protection products has done “worse than expected” through the first half of the year, with 50% of respondents saying this has been the case. Another 28% of the nation’s top ag retailers say that their seed sales have suffered thus far during the growing season.

For the crop protection products category, this underperformance in the market so far seems a bit surprising, especially with what CropLife 100 ag retailers say is one of the key issues facing their grower-customers in 2020 — herbicide-resistant weeds. According to the International Herbicide-Resistant Weed Database, there are currently 512 unique cases of herbicide resistant weeds around the world, represented by 262 separate species. In total, these weeds have developed resistance to 23 of the 26 known herbicide modes of action, which impacts more than 160 different herbicides. For example, in the U.S. during 2019, there were an estimated 50 million acres of U.S. cropland infested with herbicide-resistant waterhemp and 45 million acres that contained herbicide-resistant Palmer amaranth.

And CropLife 100 ag retailers and their grower-customers have noted these increased numbers as well. According to the 2019 CropLife 100 Mid-Year Survey, 59% of respondents said herbicide-resistant weeds were “a major problem” in their areas of the country. Another 41% said they were only “a minor problem” or “no problem at all.”

And CropLife 100 ag retailers and their grower-customers have noted these increased numbers as well. According to the 2019 CropLife 100 Mid-Year Survey, 59% of respondents said herbicide-resistant weeds were “a major problem” in their areas of the country. Another 41% said they were only “a minor problem” or “no problem at all.”

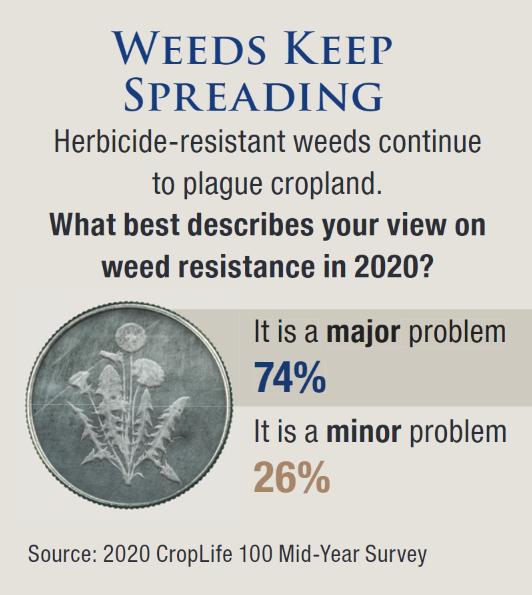

But in 2020, these percentages changed quite a bit. Today, 74% of the nation’s top ag retailers say herbicide-resistant weeds are a “major problem” for them. Only 26% say they remain “a minor problem.” Perhaps most significantly, not a single CropLife 100 ag retailer that returned the 2020 Mid-Year Survey said herbicide-resistant weeds were “no problem” for them.

Weed Worries

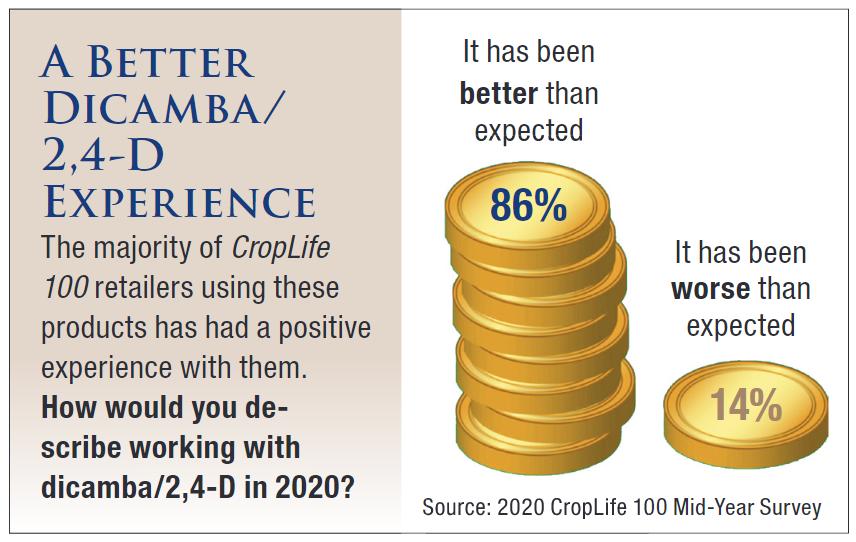

One of the newer set of tools ag retailers have utilized on these herbicide-resistant weeds in recent years involves the use of cropping systems tied to dicamba and 2,4-D. Although not widespread, with only 35% of 2020 CropLife 100 Mid-Year Survey respondents actually employing these products in their grower-customer crop fields, an impressive 86% say working with these herbicides has been “better than expected.” Only 14% of respondents said their experiences with these brands was “worse than expected.”

“Dicamba is a useful tool in our plans to control tough weeds in our growers’ fields,” said AFS’ Co-Owner Amy Asmus in a recent interview with CropLife® magazine. “Like all tools, we have to make sure we are using the right tool(s) for the job. We see our role as helping make sure growers know how to use that tool correctly and according to label directions. That includes making sure our grower applicators have the correct applicator license; complete the required trainings; use proper setbacks; have access to the approved sprayer tips; use only approved tank-mix partners; follow resistance best management practices; and use dicamba in an IPM-based plan. It is important to us and our growers that everyone stewards the tools we have so they make on-target applications and not end up where they are not supposed to be.”

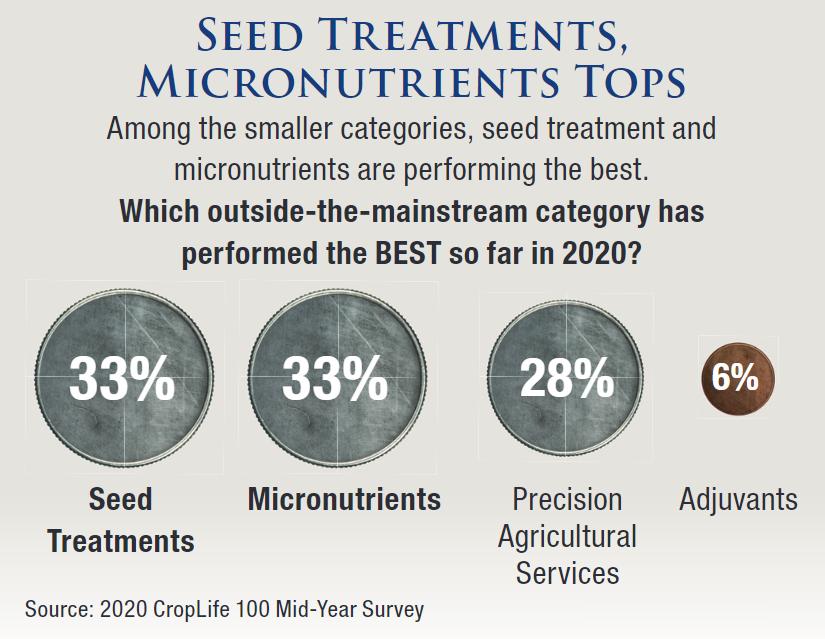

Outside of the major crop inputs/services offered by ag retailers, the 2020 CropLife 100 Mid-Year Survey asked respondents to indicate how the smaller areas of their businesses were performing in terms of dollars thus far this growing season. According to the 2019 CropLife 100 Mid-Year Survey results, precision agricultural services/products performed best during last year for the nation’s top ag retailers, with 41% saying sales for this sector were “stronger than expected.” A distant second and third were seed treatments and micronutrients, at 29% and 24%, respectively.

But in 2020, the race between these three sectors in terms of financial growth is a bit more even. According to the 2020 CropLife 100 Mid-Year Survey, 66% of respondents say seed treatment and micronutrients sales have been “better than expected” this year, at 33% apiece. Meanwhile, 28% of ag retailers say precision agricultural services are still tops for their operations.

Looking Ahead

Looking Ahead

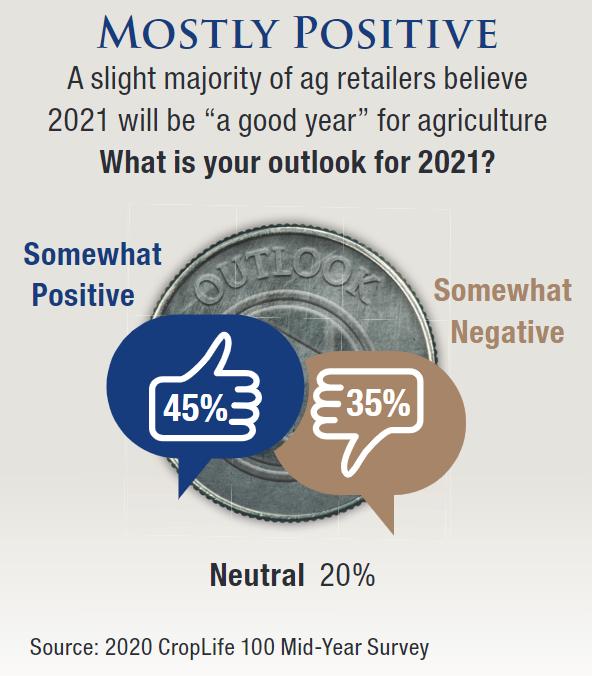

While most of the nation’s top ag retailers and their grower-customers seem relatively confident that they can manage all the change dropping onto the world during the 2020 growing season, their outlook for the 2021 growing season appears to be a bit more reserved at the moment. According to the 2020 CropLife 100 Mid-Year Survey, only 45% of respondents feel that next year’s crop year will be “somewhat positive” for their bottom lines. Thirty-five percent are convinced the 2021 growing season will be “somewhat negative” for their companies. The remaining 20% of respondents are thus far neutral in their views for next year. Perhaps significantly, no respondents to the 2020 CropLife 100 Mid-Year Survey thought 2021 would be “very positive” or “very negative” in terms of finances.

Of course, one of the big potential wild cards in this outlook for 2021 — and the rest of 2020, for that matter — remains the coronavirus pandemic. According to the 2020 CropLife 100 Mid-Year Survey, a full 90% of respondents believe COVID-19 will have some kind of “negative financial impact” on their businesses by the end of 2020. Half, 50%, of respondents say they are “somewhat concerned” when it comes to the coronavirus outbreak and its ultimate financial toll. Another 40% say they are “very concerned” regarding their finances because of COVID-19. Only 10% say the pandemic will have “no impact” on their financial growth by the end of the year.

Subscribe Today For