2018 Buying Intentions Survey: Good News for Fertilizer and Crop Protection; Flatness Elsewhere

January 11, 2018

January 11, 2018 Another flip of the calendar and a new growing season is upon us! As the ag retail marketplace enters 2018, many out in the supplier world are anxiously asking the same time-honored question: Will my products be in demand this year, or should I start planning now for a better year once this one has ended?

Four years ago, CropLife® magazine was pondering this same question on behalf of dozens of suppliers/advertisers with the desire to find out some answers. So we formulated and distributed the very first Buying Intentions Survey. This short (11 questions) form asked those in the ag retail industry to tell us in what product categories they expected to spend the majority of their budgets on for the upcoming growing season. Since that time, the results from this annual survey have become a regular part of CropLife’s annual State of the Industry report in each and every January edition of the magazine.

Now, onto a look at the 2018 edition of the Buying Intentions Survey results. First, however, some particulars. The 2018 Buying Intentions Survey was taken by 411 respondents during a two-week period in early November 2017. In all, the majority of these described themselves as ag retailers (79%). Another 8% indicated their primary business as equipment dealers. The remaining 13% split almost evenly between fertilizer producers (4%), manufacturers/ formulators (5%), and research representatives (4%).

Undoubtedly, most observers to the ag retail market are probably wondering if the relatively humdrum spending habits that have been the norm since the end of 2013 will begin to show some across-the-board improvement. The short answer appears to be “no.” Providing a quick summation of the findings, the majority of 2018 Buying Intentions Survey takers generally plan to spend the same amounts they did during 2017 for the majority of their crop inputs/ equipment purchases. However, there are a segments where overall spending should be on the uptick, particularly in the fertilizer and crop protection categories.

The Fertilizer Outlook

There’s virtually no way to sugarcoat it — fertilizer sales have been brutal for ag retailers for the past few years. In fact, according to data from the 2017 CropLife 100 survey, the nation’s top ag retailers saw their overall fertilizer revenues drop by more than $1 billion last year, topping out $12.1 billion. But there is some hope on the horizon when it comes to fertilizer spending for 2018.

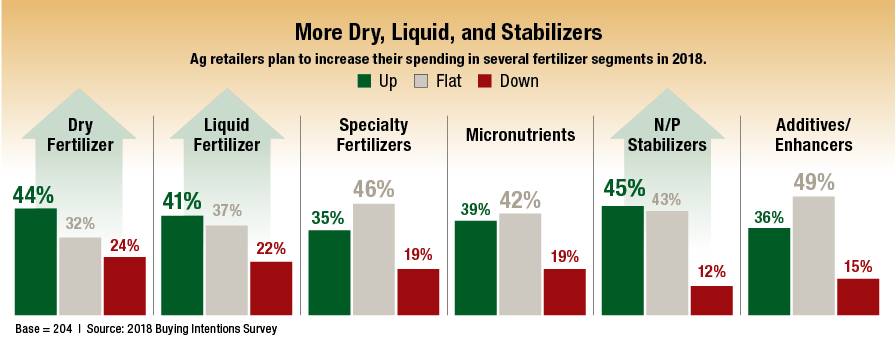

According to the 2018 Buying Intentions Survey, three of the six segments tracked — dry fertilizer, liquid fertilizer, and, nitrogen/phosphorous (N/P) stabilizers — can expect to have better spending figures this year than in the previous year.

Leading the pack in planned spending for 2018 are N/P stabilizers. As more and more grower-customers look to optimize their macronutrient crop uptake in the field, they are apparently increasingly using products in this segment to accomplish this. According to the survey, 45% of respondents are planning to increase their spending in the N/P stabilizers segment between 1% and more than 11% this year. This is a healthy 12% increase from the 2017 survey total of 32%. A slightly smaller percentage, 43%, say that their spending in this area will be the same as it was in 2017. In the 2017 survey, flat spending for N/P stabilizers lead among all percentages at 46%.

Finishing a close second in fertilizer planned spending for 2018 are dry fertilizers. During the 2017 Buying Intentions Survey, 42% of respondents indicated they planned to increase their spending in this area between 1% and more than 11%. For 2018, this percentage has improved 2% to 44%. Another 32% plan to spend exactly the same amount on dry fertilizers as they did the prior year — the same percentage as the category recorded for the 2017 survey.

As for the liquid fertilizer segment, this also recorded a 2% gain in the number of ag retailers planning to increase their spending 1% to more than 11%, from 39% in 2017 to 41% for 2018. As with the dry fertilizer segment, the percentage of respondents planning to spend the same amount on liquid fertilizer offerings stayed flat at 37%.

For the other three fertilizer segments — micronutrients, specialty fertilizers, and additives/ enhancers — the number of ag retailers planning to keep their spending flat outnumber those that plan to increase theirs. But the percentages are not that far apart. For example, while 42% of respondents are keeping their micronutrients spending flat, 39% are planning a 1% to more than 11% increase. The situation is similar for both specialty fertilizers (46% plan no increased spending vs. 35% that do) and additives/enhancers (49% plan no spending increase vs. 36% that are planning to spend more).

The Crop Protection Products Outlook

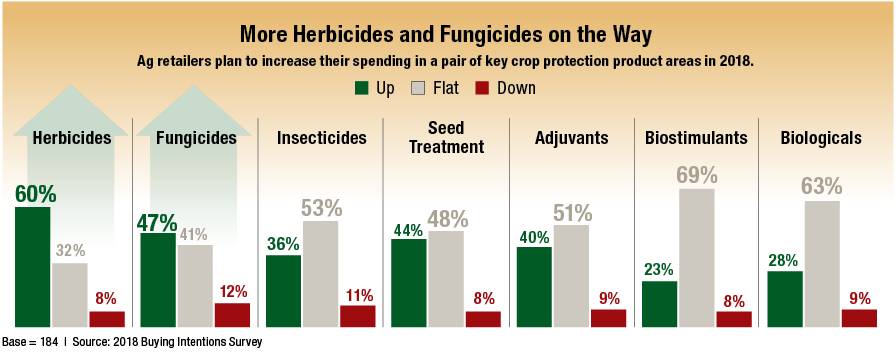

In stark contrast to the fertilizer category, the crop protection products market has been on a roll the past few years. In 2017, for example, sales in this category among CropLife 100 retailers grew 14% to hit $11.4 billion. Leading the charge forward has been the herbicides segment, as grower-customers look for new and different options to combat a growing host of herbicide-resistant weeds. In the 2017 Buying Intentions Survey, 47% of respondents said they were going to spend more money in the herbicides segment than during the prior year.

And this trend will likely continue into 2018 as well. According to the 2018 Buying Intentions Survey, 60% of respondents are planning to increase their herbicide spending 1% to more than 11%. Better still, only 8% are planning to decrease their spending in this area, a drop of 10% from the 2017 survey’s 18% mark.

A similar buying profile also seems likely for the fungicides segment. Here, 47% of 2018 Buying Intentions Survey respondents plan to increase their spending vs. 2017, perhaps spurred on by wet/cool conditions across much of the country leading to increased disease pressures over the past two growing seasons. Another 41% plan no increased spending, with the remaining 12% planning to cut spending in this segment between 1% and more than 11%.

If there’s a dark spot for the crop protection products category in 2018, it could be insecticides. In this segment, only 36% of 2018 Buying Intentions Survey respondents plan to up their spending. More than half, 53%, plan no spending increases this year for insecticides.

As for the other four segments tracked in the crop protection products category on the survey — seed treatment, adjuvants, biostimulants, and biologicals — all four seem destined to see flat spending in 2018 vs. 2017. Based upon the 2018 Buying Intentions Survey results, seed treatment will perform the best, with 44% of respondents planning to increase spending while 48% plan to spend the same amount as they did in 2017. The worst performer will be biostimulants, where only 23% of survey respondents planned to up their spending between 1% and more than 11% in 2018. The vast majority, 69%, are planning no biostimulants purchase increases for the year.

For adjuvants, market dynamics look similar to seed treatment, with 40% increasing their spending and 51% spending the same amounts as in 2017. Meanwhile, 28% of 2018 Buying Intentions Survey respondents plan to spend more on biologicals this year, with 63% spending the same, and 9% spending less — essentially mirroring the spending plans for the biostimulants segment.

The Seed Outlook

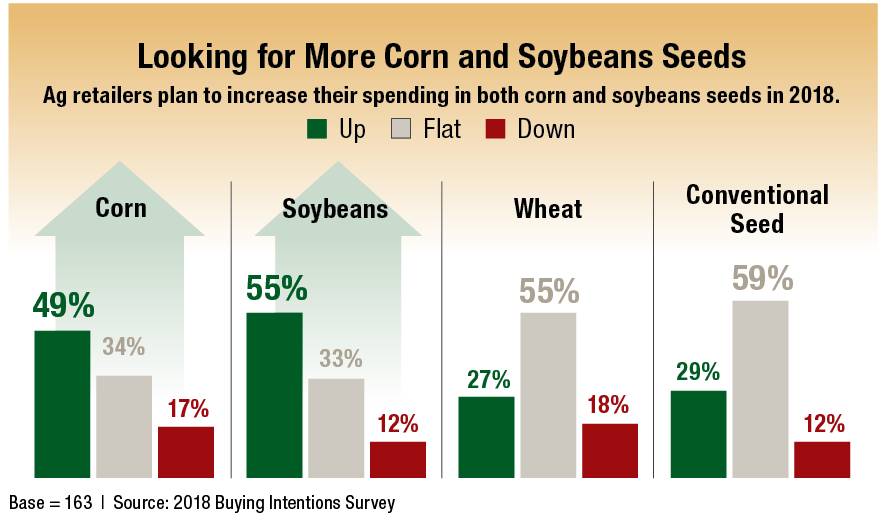

Going into the 2017 season, that year’s Buying Intentions Survey predicted the seed category would see some moderate decreases in spending for the year. And this seemed to be the case. According to the 2017 CropLife 100 survey, seed sales grew a modest 2% for the year, topping $4.7 billion. But early indications are that 2018 could be a slightly better sales year for seed, particularly when it comes to corn and soybean seeds.

According to the 2018 Buying Intentions Survey, 49% of respondents plan to increase their spending on corn seeds between 1% and more than 11% for the year. This compares with 36% that increased their spending in this segment during 2017. For soybean seeds, 55% of respondents are looking to up their spending, a slight drop of 1% from the numbers recorded in the 2017 survey. In both segments, approximately one-third of respondents anticipate keeping their corn and soybean seed spending flat from 2017 (34% and 33%, respectively).

For wheat seed sales, the outlook is a bit more conservative. For 2018, only 27% of Buying Intentions Survey respondents expect to increase their spending for wheat seeds between 1% and more than 11% for the year. More than half, 55%, plan no increased spending in this segment and 18% expect to spend less on wheat speeds.

The breakdown is similar for conventional seeds. According to the 2018 Buying Intentions Survey, 29% of respondents will be spending 1% to more than 11% more on conventional seeds this year. However, 59% will keep their spending amounts at the same level as in 2017 with the remaining 12% cutting this segment’s sales between 1% and more than 11%.

Equipment Outlook

Finally, there is the expected outlook for the equipment marketplace. Based upon the number of new product introductions at the 2017 summer trade shows, equipment manufacturers from all sectors are anticipating 2018 will be a big year for product demand from ag retailers.

“It’s been a long time since I’ve seen so many new pieces of equipment being launched into the market at the same time,” observed Mark Burns, Marketing Manager for Application Equipment at Case IH while attending the 2017 Agricultural Retailers Association meeting in Phoenix, AZ. “I think a lot of companies are expecting a strong year in 2018.”

But are these expectations being borne out by the results from the 2018 Buying Intentions Survey? In a few words, not really.

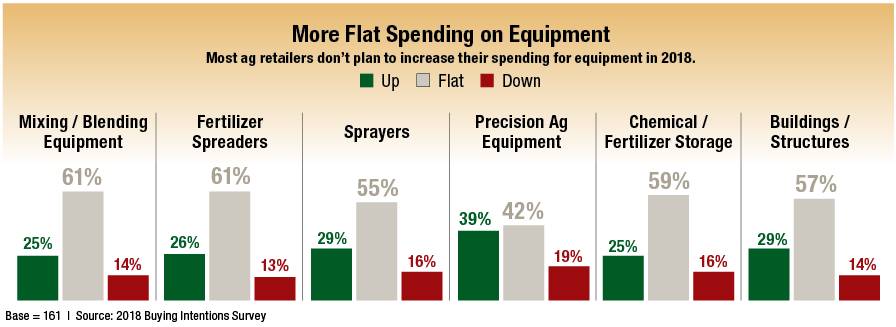

Take self-propelled sprayers, for example. During the past few months, approximately half-a-dozen companies have introduced new or upgraded models for this market — and a few more are on the way for the 2018 growing season as well. Yet, according to the survey, only 29% of respondents plan to increase their spending on sprayers between 1% and more than 11%. A much larger percentage, 55%, plan to keep their sprayer spending at their 2017 levels, with the remaining 16% decreasing their spending in this segment.

The numbers are similar for both the fertilizer spreaders and mixing/blending equipment categories. For spreaders, 26% of 2018 Buying Intentions Survey respondents plan to grow spending in this segment. For mixing/blending equipment, the percentage planning spending increases in 2018 stands at 25%. In both segments, 61% of respondents are looking for no spending increases in either segment for the year.

In the area of precision agriculture equipment, the percentages are virtually the same. According to the survey, 27% of respondents plan to up spending in this segment during 2018. Sixty-three percent are budgeting for no increases in their precision agricultural equipment spending, with the remaining 10% planning to cut spending in this area.

Finally, when it comes to storage and structure build-outs, the anticipated spending profiles are also in the mid to high 20% ranges. For chemical/fertilizer storage, 25% of 2018 Buying Intentions Survey respondents expect to spend more money than they did in 2017. The remaining groups plan to keep their spending at their 2017 levels (59%) or decrease spending in this area (16%).

For buildings/structures, the percentages are slightly better. Here, 29% of survey respondents are planning to increase their spending between 1% and more than 11%. Fifty-seven percent see no spending growth in this segment, while the remaining 14% will be spending between 1% and more than 11% less for their buildings/structures demands.

Subscribe Today For