In Crop Protection, America First

November 27, 2017

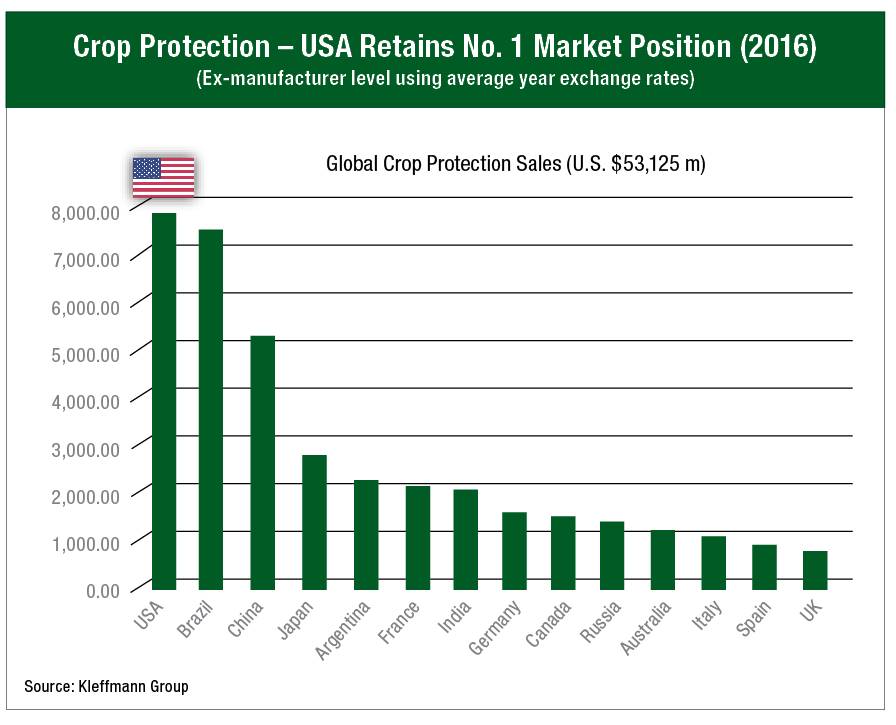

November 27, 2017 In nominal terms, the global market for crop protection chemicals further declined to $53.1 billion in harvest year 2016 as measured at the ex-company level and using average year exchange rates throughout. This represents the second year of decline in the global market. The rate of decline, however, has slowed with the big drop of some 9.8% in 2015 as compared to 2014 coming down to a more modest decline of some 2.6% in 2016 as compared to 2015. A recovery from this now low base of just over $53 billion should be more readily achieved. The question remains as of to what extent that growth returns already in 2017.

As in the previous year, no region escaped the global pressures on the market although in contrast to 2015 no region saw an overall drop in market value of greater than a few percentage points. In general the market was a lot “flatter” with declines seen across the board as markets stabilized from the previous years’ decline. There were of course a few notable exceptions of growth; including the markets of Russia, Japan, India, and Argentina.

U.S. Still in Front

The U.S. fell “into the bucket” of small to moderate decline broadly in-line with the overall global market decline. Once again, the U.S. market fell from just over $8 billion to just over $7.8 billion, a decline of a fraction over 2%. Despite this, the U.S. retained, for the second year running, its position as the leading global crop protection market in terms of sales. A decline of some 4.8% in the Brazilian market meant that the gap between these two leading markets widened from under $100 million in 2015 to close to $300 million in 2016.

While the difference in value of some $300 million is not earth-shattering, it does indicate the different fortunes of the world’s largest two markets. Of course the “devil is in the details” (currency movement being once again the biggest devils here) and there are different ways to paint quite a different story. One such way is to look at the two markets in terms of area treated. If we compare the cumulative acres of product used on the ground then Brazil continues to grow with in 2016 over 2.7 billion acres (super developed area) treated.

The U.S. by comparison remained essentially the same in 2015 with a little over 1.2 million areas treated; and by those calculations; under half of that of Brazil. For now, however, Brazil continues to suffer from ongoing challenges including currency movement, credit availability and pricing pressure, which “dampen” the intrinsically higher potential of this market.

Compared to other sectors in the industry a decline of 2% in the value of the U.S. crop protection market was extremely modest. Taking the latest USDA estimates, the U.S. net farm income — a key indicator of U.S. farm well-being — stood at $61.5 billion in 2016 as compared to $81.4 billion in 2015; a substantial decline of 24%. While not strictly comparable in that the livestock sector fared the worst, it is an indication that the crop protection sector performed relatively well under such an environment. Although subject to revision the current USDA study puts the U.S. net farm income in 2017 at $63.4 billion in 2017, up 3% from 2016. The forecast rise in 2017, closely linked to commodity prices, comes after three consecutive years of decline, from the 2013 record high of $123.8 billion, and could indicate the first “green shoots” of an improving U.S. farm economy.

The Category Breakdown

The 2% decline in the U.S. market was not universally felt in the different product groups of herbicides, insecticides, and fungicides.

■ Fungicides. Fungicides which had been the shining star in the U.S. market in 2015 (where the weather patterns favored the use of fungicides) shrunk such that the market was a little over $1.1 billion as compared to $1.2 billion in 2015. Despite the decline experienced in 2016, the sector is, however, poised for growth as co-formulations with the relatively new SDHIs continue to “prove” themselves. While fungicides remained the “easy option” to cut from the spray program in 2016, even a small improvement in the commodity price situation favors the use of the higher value SDHIs in a market that remains dominated by single active ingredient-based products such as those based on triazoles or strobilurin.

■ Herbicides. Herbicides, by far the largest sector within the U.S. market, saw somewhat of a reversal of fortunes in 2016 as compared to 2015 growing some 1.5% to reach $4.6 billion. The dominant herbicide markets of corn and soybean both drove this forward as growers increasingly moved to greater use of residuals and pre-emergence products. In soybeans, glyphosate-based products still dominate, but the soybean “residual” pre-mixes based on sulfentrazone, chloransulam, and chlorimuron are gaining a larger part of the cake.

New technologies from 2017 with for example some 20 million acres of Xtend (dicamba-tolerant) soybeans already planted are changing that dynamic once again somewhat. The subject of much debate, current “teething” problems with dicamba drift, one way or another will impact on the acceptance of that technology, the competitive Enlist (2,4-D) technology, and on late pipeline developments such as those based on HPPD-inhibiting herbicides.

■ Insecticides. Insecticides also saw a decline in 2016 dropping 6% to $1.8 billion. Here the decline was felt across virtually all crop groups with the exception of cotton, which improved largely on the back of increasing planted areas. In addition, the sector (still dominated by older generic organophosphate and pyrethroid chemistries such as dicrotophos and bifenthrin) is benefiting from formulation based on newer active substances including spiromesifen and flupyradifurone.

Subscribe Today For