Smart Tech

2026 CropLife/Purdue Survey Reveals Shifting Priorities in Precision Agriculture

July 1, 2026

July 1, 2026 Editor’s note: The CropLife/Purdue Precision Survey is the longest-running continuous study of precision ag adoption, conducted now for three decades — at least every other year since 1996. The 96 ag retailer input supplier respondents were mostly located in the Midwest and included cooperatives, independent retailers, and those part of a regional or national chain. The results reported are for dealers that identified as primarily working with field crops such as corn, soybeans, wheat, rice, cotton, milo, sugar beets, and forages. Dealers that work with specialty crops such as tree fruits and nuts, vegetables, berries, and grapes were analyzed separately.

![]() Be First to Hear the 2026 Precision Ag Dealership Survey Results

Be First to Hear the 2026 Precision Ag Dealership Survey Results

Join us at 2026 Tech Hub LIVE as Purdue’s Bruce Erickson unveils the latest Precision Agriculture Dealership Survey findings. Learn more >>

Recent months have been times of uncertainty for much of U.S. agriculture, with grain exports, fertilizer and fuel prices, and labor among the issues impacting crop producers and their input suppliers. This uncertainty seems to be reverberating in digital agriculture as well, with field crops retailers re-evaluating their strategy. Some long-time precision farming services are being dropped, while some new products and services are being added. Dealers are critically evaluating the potential for recent innovations like artificial intelligence, machine vision, and automation/robotics.

Crop Inputs with Drones a Growing Market Factor

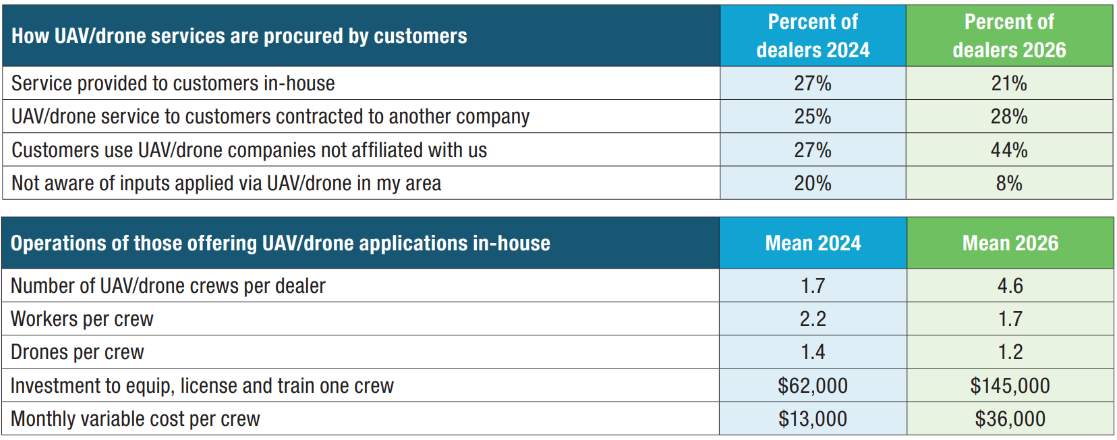

More than 90% of dealers know of UAV input applications in their market area. Half of dealers say they offer crop inputs to customers with drones, either as an in-house service or contracted to another company. Competition from independent UAV service providers seems to be increasing sharply.

Dealers report costs have gone up markedly since 2024, although the number of responses is small, only for those providing these services. Dealers said setting up a crew costs an average of around $145,000, to equip, license, and train. And it costs around $36,000 per month to keep each crew running — the variable costs which could include wages, fuel, repairs and maintenance, insurance, etc. Dealers doing their own in-house drone spraying have, as an average, added more crews. This is only the second time this question has been asked, so we are making no claims about establishing benchmarks or seeing a trend develop.

In 2024, dealers offering drone services indicated that around two-thirds of applications were for fungicides on corn, around 13% herbicide applications in pastures and fencerows, approximately 10% for insecticide applications on corn, and about 6% for insecticide applications on soybeans.

Dealers Are Evaluating the Benefits of Automation and AI

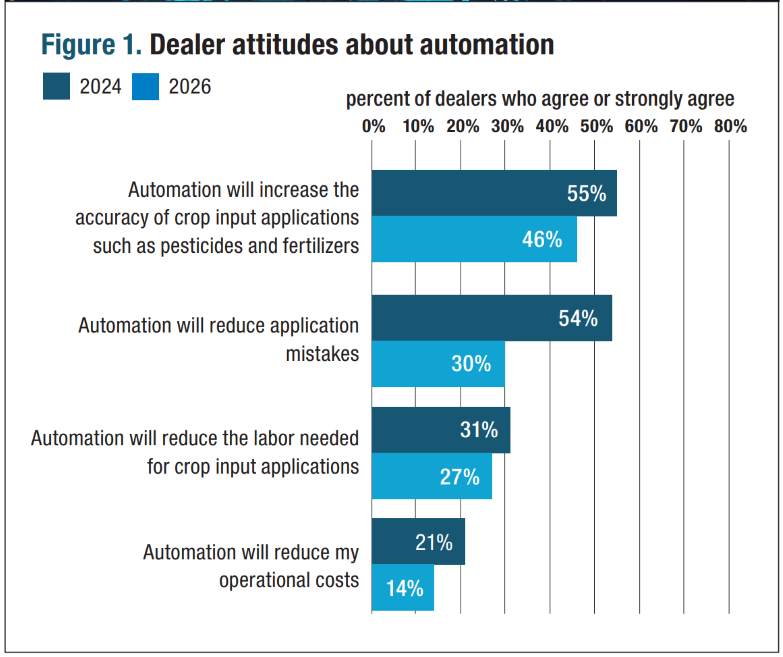

Two years ago, dealers were asked how they thought automation/robotics might affect their businesses, and we asked that question again in 2026. Automation is already widely used in crop production — for example, in boom/nozzle controllers and autosteer — but appears poised for greater expansion. Around half of dealers think that automation/robotics will increase the accuracy of crop input applications (see Figure 1 below) — but fewer dealers say automation will reduce application mistakes. Less than a third of dealers indicate automation will reduce their labor needs associated with crop inputs, and many fewer think it will reduce costs. To some the labor response may be a surprise, as labor savings is often viewed as the most obvious result of automation — to take a task out of a human’s hands that we pay to employ.

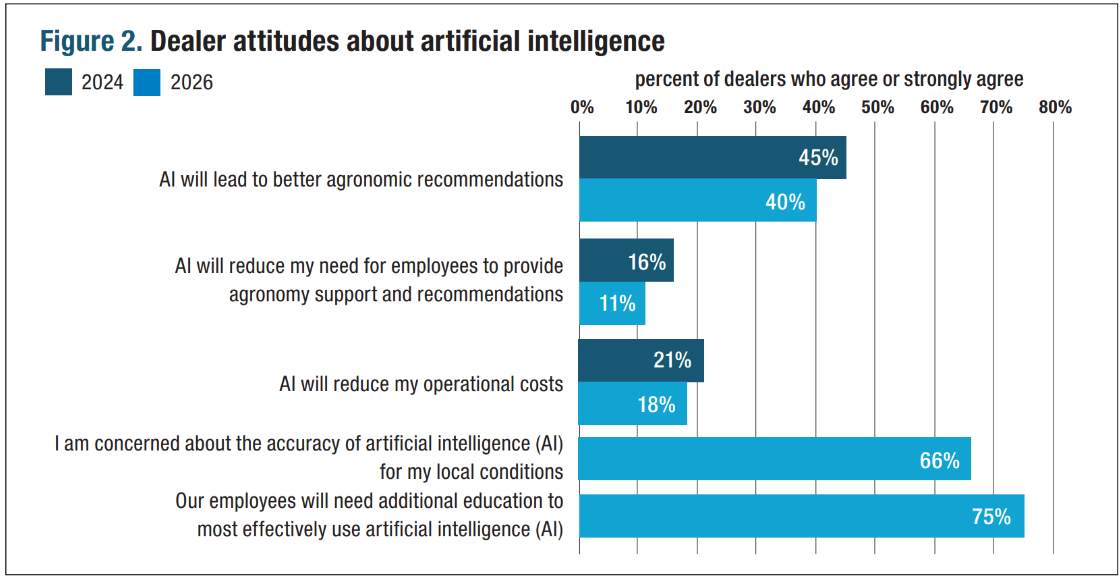

The promise of artificial intelligence (AI) dominates general U.S. business and financial news, but less than half of dealers say AI will lead to better agronomic recommendations (see Figure 2 below). Even fewer dealers say AI will reduce their operational costs, perhaps by needing fewer workers or being more efficient. Questions added in 2026 show that most dealers have concerns that AI will not capture their unique local situation, and there will need to be investments in education to get workers to effectively use AI. Dealers currently using AI indicate they use it the most for imagery analysis, and less for variable rate prescription generation, agronomic recommendations, logistics/routing of equipment, and customer relationship management.

Questions About Profits in Precision Farming

Dealers were asked how their revenue from precision products and services changed in the last three years. Thirty-eight percent responded with about the same, nearly half said revenue was up, and 12% said down.

And while revenues are up, so are expenses. As a simple, non-weighted average of all precision products and services, the dealers offered, 54% of dealers said they were at least breaking even in 2026; lower than 67% in 2020, 64% in 2022, and 66% in 2024. Dealers have long indicated, as an average, that their precision products and services were not making a profit, but at least most were breaking even — a profitability question has been a part of the survey since its beginnings. Dealers indicate the most profit with fertilizer-related offerings such as soil sampling and variable rate technology fertilizer applications, a situation seen for many years.

The technologies with the greatest number of dealers not breaking even are for relatively new technologies, including UAV or drone imagery, where one-fourth show a loss, and machine vision weed detection on sprayer, with one-third showing a loss.

In addition to dealers indicating lower profits, more dealers say they don’t know. Again as a simple non-weighted average of all technologies asked, 35% of dealers say they did not know the profitability in 2026, compared to just 17% in 2020, 23% in 2022, and 13% in 2024. Understandably, the greatest uncertainty that most respondents don’t know is with newer precision ag such as robotic crop weeding and scouting, and machine vision weed detection on sprayer, where half of the dealers responding didn’t know. This is not surprising, as new offerings may not be particularly profitable or dealers may not know in the first few years, as it takes time for dealers to gain experience and for farmers to learn about possible benefits.

A full report detailing all of the 2026 results will be posted on CropLife.com later this year. The full report from the 2025 survey, and also previous years, can be accessed here.

For more Smart Tech topics, click here.

Subscribe Today For