Precision Agriculture Survey: Ag Retailers Share What They Think About AI, Drones and Other Technologies

July 15, 2024

July 15, 2024 Editor’s note: The CropLife/Purdue Precision Survey is the longest-running continuous study of precision farming adoption, conducted at least every other year since 1996. The 108 agricultural retailer input supplier respondents mostly from the Midwest included cooperatives, independent retailers, and those part of a regional or national chain. Those answering as a farm equipment dealer or consultant in the first question were not allowed to continue. The results reported are for dealers that identified as primarily working with field crops such as corn, soybeans, wheat, rice, cotton, milo, sugar beets, and forages. Dealers that work with specialty crops such as tree fruits and nuts, vegetables, berries, and grapes are analyzed separately.

View all

New forms of digital technology are making their presence known on farms and the businesses that support them, according to data from 2024 Precision Agriculture Dealership Survey. These include new applications of automation, using UAVs/drones for input applications, and of course artificial intelligence (AI) — where everyone wants to play now! Who is using them, and why? Understanding their use and value can seem more complicated than our more familiar precision practices. In recent years we have reported mostly on long-time, foundational precision ag — yield monitors/mapping, GPS guided precision soil sampling, variable rate applications, satellite/aerial imagery, auto guidance, all originating in the 1990s. With many of the foundational technologies either maturing with widespread adoption or in a state of stagnation, for the 2024 survey we decided to focus more on the new and what is possibly headed our direction.

Adoption of the New

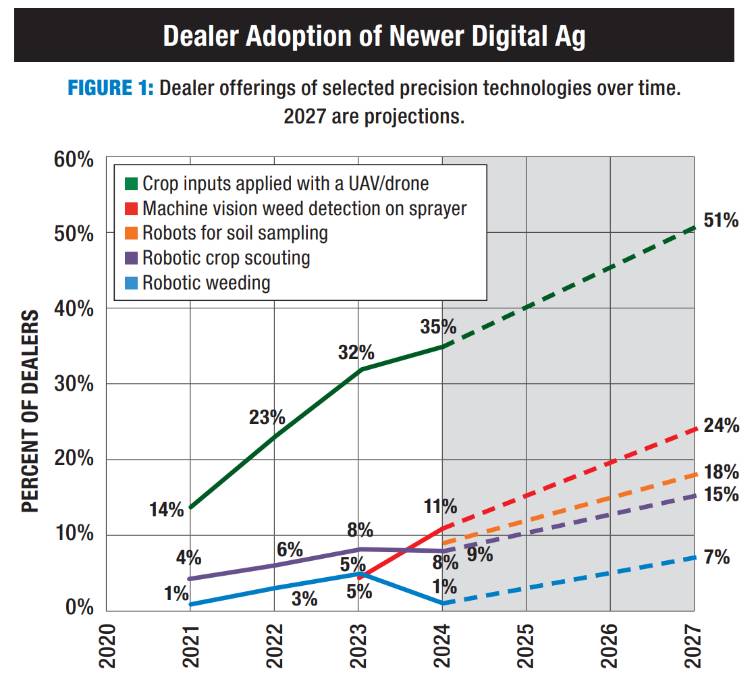

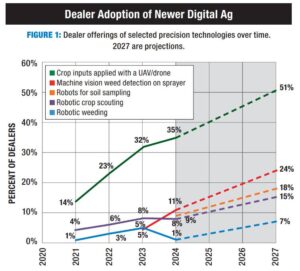

Many dealers have plans for these new technologies (Figure 1). About a third say they are currently offering crop inputs (such as a pesticide) applied with a UAV/drone — but fully half say they will be offering this in three years, a remarkable rise from three years ago. Robotics for soil sampling, crop scouting, and for crop weeding are only offered by a small percentage of dealers now, but more dealers plan to offer these in the future. Artificial intelligence that identifies weeds for spraying is offered by just 11% of dealers now, but a quarter say they will offer this service three years out.

Attitudes on Automation/Robotics

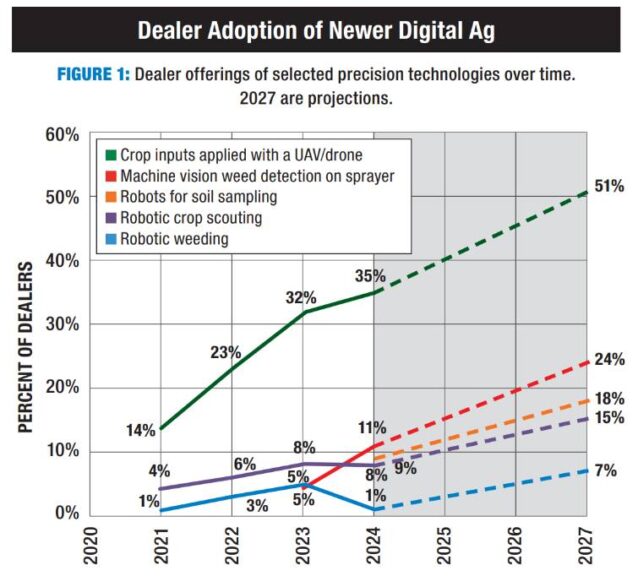

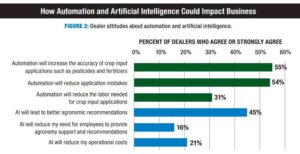

Dealers were asked how they thought automation/robotics might affect their businesses. Automation is already widely used in crop production — for example boom/nozzle controllers and autosteer but appears poised for greater expansion. Most dealers think that automation/robotics will increase the accuracy of crop input applications (Figure 2) — indeed it already has with section controllers, and the planter row controllers and variable rate downforce used by their farmer customers. And most dealers say automation will reduce application mistakes. But less than a third of dealers indicate automation will reduce their labor needs associated with crop inputs. To some this may be a surprise, as labor saving is often viewed as the most obvious result of automation — to take a task out of a human’s hands that we pay to employ!

Dealer Thoughts on Artificial Intelligence

Dealers were asked how they thought AI might affect their businesses. Almost half of dealers say AI will lead to better agronomic recommendations. That makes good sense and comes at a good time. It seems we have been at an impasse on agronomic recommendations for many years. With fertilizers, we are following recommendations that in some cases have been around for decades. Many new methods have not had the impact we thought they might — such as greenness / chlorophyll sensors, or electrical conductivity measurements (EC). And we are not even close at making full use of yield maps or field imagery, in measuring field variability then acting upon it. We need that “next thing” that will move us forward.

At the same time, few dealers say AI will reduce their need for agronomic expertise, or reduce their operational costs, perhaps by requiring fewer workers or being more efficient. Perhaps dealers’ thinking aligns with how previous technologies have affected the workplace. Long ago mechanization, computers, pesticides, and other labor-saving devices were expected to bring in a new era of less work. It didn’t always end that way at all, as workers in many cases were just expected to do more or were assigned to other tasks.

UAV/Drone Applications

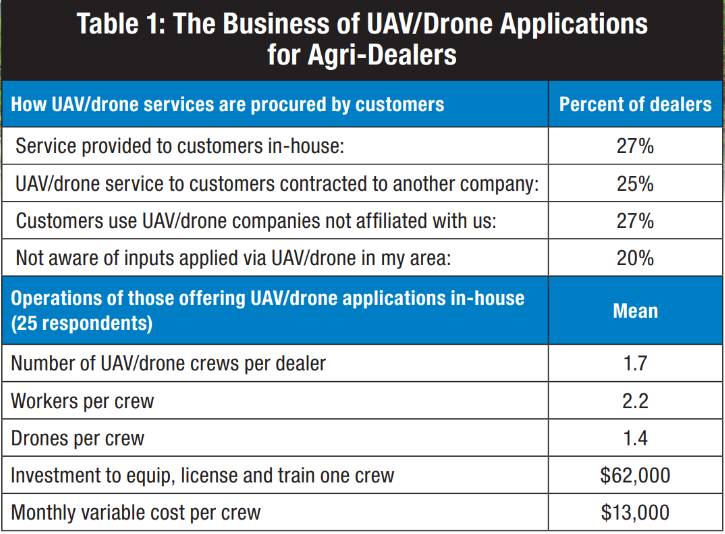

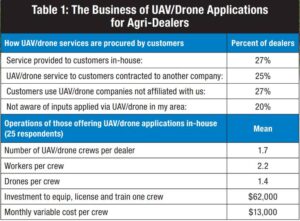

About one-fourth of the dealers reported that they provide UAV/drone application services in-house, and another 25% say they contract this to another company (Table 1). For those providing the services, the average number of crews used was about two, with each having two workers and one or two drones. Dealers said setting up a crew costs an average of around $62,000, to equip, license, and train. And it costs around $13,000 per month to keep each crew running — the variable costs, which could include wages, fuel, repairs and maintenance, insurance, etc. This of course needs to be compared to the revenues from these services, and the alternative costs in most cases of owning and operating a ground sprayer or hiring an aerial applicator, each of which involve considerable expense.

Profitability Of Precision Offerings

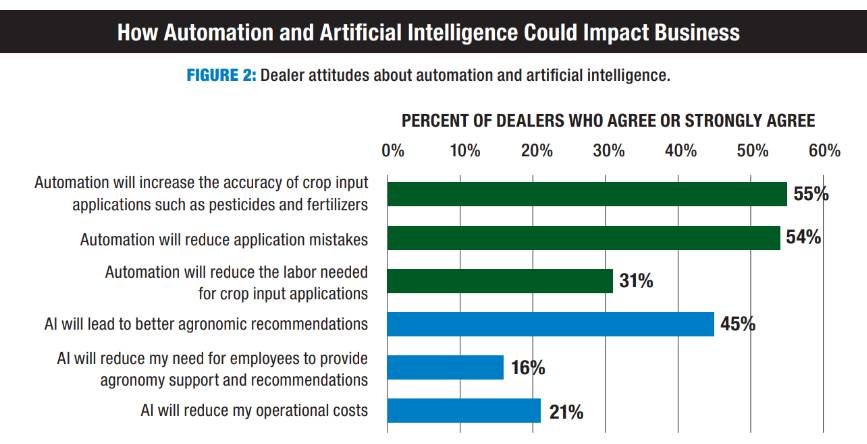

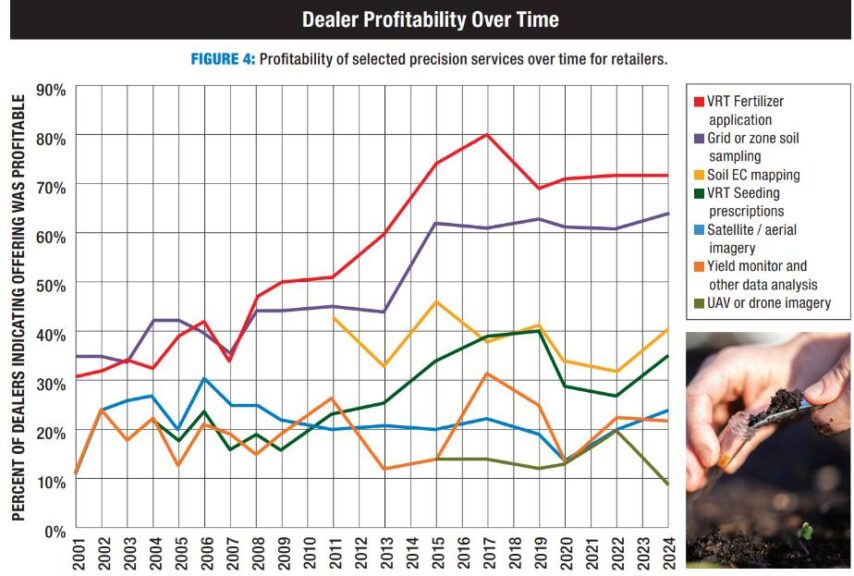

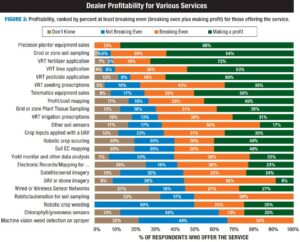

The 2024 CropLife/Purdue Precision Survey showed that dealers are not making a profit on most of their precision products and services, but they are at least breaking even on all except some of the newest (Figure 3). As has been the situation for many years, crop nutrient management services are some of the most profitable, with 64% of dealers saying their precision soil sampling is profitable, as well as 72% with their precision fertilizer applications. Precision planter equipment sales, VRT liming, and VRT pesticides were also profitable for most dealers that offer them. On the low end of profitability were imagery services such as from satellite, aerial, and drone/UAVs, where most dealers said they were at least breaking even, but far more reported losing money as compared to making a profit. Profit can be difficult to fully assess, as fixed costs may be spread among multiple enterprises and offerings. And a dealership may accept an unprofitable activity to enable a profitable one, i.e., a loss leader, or to compete with other neighboring dealers for farmer business.

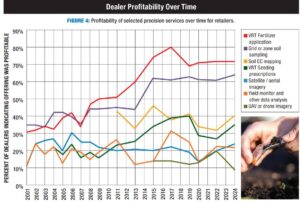

Precision nutrient sampling and precision fertilizer applications have been profitable for dealers for over a decade, while imagery offerings and yield monitor analysis have not been profitable (Figure 4).

Subscribe Today For