The 2024 CropLife 100: Weathering a Rough Year in Ag Retail

December 4, 2024

December 4, 2024

As a snapshot of what’s going on in the ag retail business, the annual CropLife 100 report can be incredibly insightful. Of course, not every growing season tells a positive story — at least at first glance.

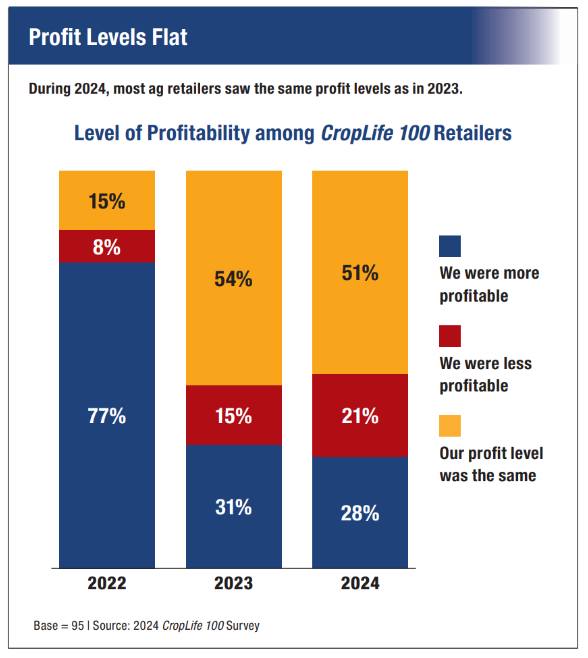

And at first glance, the 2024 growing season was not one the nation’s top ag retailers will remember fondly. According to the 2024 CropLife 100 survey, the largest ag retailers recorded revenues totaling $43.3 billion this year. While an impressive number by itself, this represented a $3.4 billion decline from the 2023 totals, a 7.2% drop.

For the most part, virtually all of the members of the CropLife 100 experienced a down revenue year in 2024 vs. 2023. This represented quite a change from just a few years ago. For instance, back in 2022, 99 out of the 100 nation’s top ag retailers saw sales increases year-over-year for their crop inputs/services offerings. In 2024, the number of CropLife 100 ag retailers recording sales gains for the year was only 15. The vast majority — 57 — saw across the board sales declines this growing season. The remainder had flat sales.

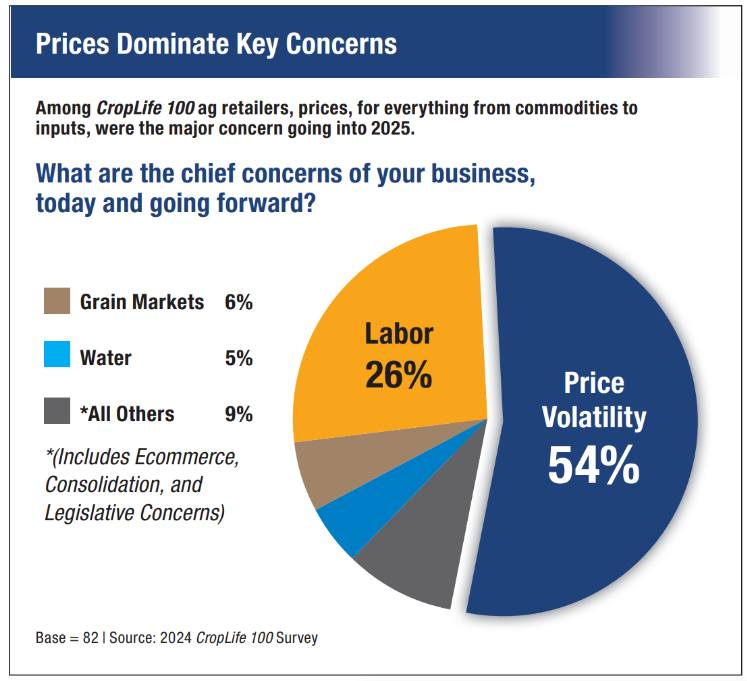

Perhaps not surprisingly, this “concern” over prices also came through loud and clear in the overall 2024 CropLife 100 survey results. In most years, when ag retailers are asked what their major concerns/worries are and are expected to be during the upcoming growing season, finding/keeping good employees (a.k.a., labor) tends to dominate the percentages. In 2023, for example, labor worries were cited by 34% of CropLife 100 ag retailers as their top challenge going into the 2024 growing season. This far outpaced every other major concern by almost 10%.

Perhaps not surprisingly, this “concern” over prices also came through loud and clear in the overall 2024 CropLife 100 survey results. In most years, when ag retailers are asked what their major concerns/worries are and are expected to be during the upcoming growing season, finding/keeping good employees (a.k.a., labor) tends to dominate the percentages. In 2023, for example, labor worries were cited by 34% of CropLife 100 ag retailers as their top challenge going into the 2024 growing season. This far outpaced every other major concern by almost 10%.

However, according to the 2024 CropLife 100 survey, labor concerns now rank second among key challenges, cited by only 26% of respondents. Instead, 54% of the nation’s top ag retailers now say price volatility — from lower commodity prices to higher interest rates to higher crop inputs costs — is their chief concern for the 2025 growing season.

“The combined factors of rising costs, supply chain volatility, and growing demand for technology innovations are shaping a tough environment for ag retailers,” wrote Jamie Scanlon, Head of Customer Experience at Simplot Grower Solutions, on the company’s CropLife 100 form.

Ernie Roncoroni, President/CEO at Grow West, agreed with this assessment. “Stress at the grower level is unprecedented,” wrote Roncoroni on his company’s survey form. “Low commodity prices, lack of demand, high cost of doing business, liquidity issues, and regulations are all impacting growers.”

All Categories Suffer

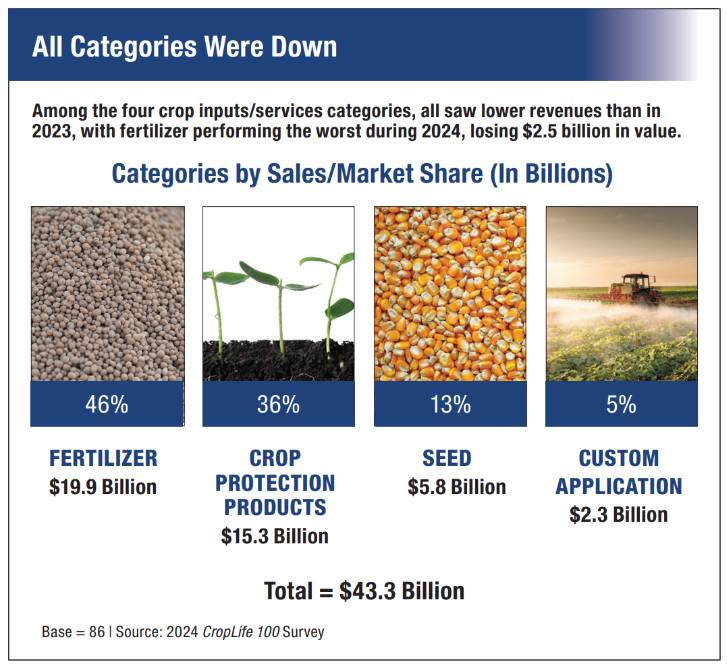

To appreciate just how deep this revenue decrease ran for the nation’s top ag retailers, consider the performances of the four major crop inputs/services categories — fertilizer, crop protection products, seed, and custom application — for 2024. In a typical year, one or two of the four categories will see some sales gains; the rest will not. This was certainly true in 2023, when three of the four categories saw revenue increases from the year before.

To appreciate just how deep this revenue decrease ran for the nation’s top ag retailers, consider the performances of the four major crop inputs/services categories — fertilizer, crop protection products, seed, and custom application — for 2024. In a typical year, one or two of the four categories will see some sales gains; the rest will not. This was certainly true in 2023, when three of the four categories saw revenue increases from the year before.

However, 2024 will go down as an exception to this rule. According to data collected in the 2024 CropLife 100 survey, three of the four categories experienced sales declines for the year. The only one not to was the seed category. Here, overall revenues in 2024 were essentially flat year-over-year at $5.8 billion. Despite this, seed was still able to increase its market share among all crop inputs/services, however, up 1% to 13%.

For the other three categories, the tally for the year was in levels of loss vs. 2023. For instance, the crop protection products category saw its overall revenue among CropLife 100 ag retailers decline $400 million, from $15.7 billion in 2023 to $15.3 billion this year. Like seed, however, the category did manage to regain some market share compared with the other crop inputs/services tracked within the CropLife 100. Overall, the crop protection products category now accounts for 36% share of all crop inputs/services, an increase of 2% from 2023.

For the remaining two categories — custom application and fertilizer — 2024 represented declines across the sales range, from actual revenues to market share. For the smallest category, custom application, 2024 was an off year. Overall, according to the survey data, revenues in this category dropped $500 million, from $2.8 billion in 2023 to $2.3 billion this year. Market share for this category also was down, off 1% from 6% in 2023 to 5%.

For the remaining two categories — custom application and fertilizer — 2024 represented declines across the sales range, from actual revenues to market share. For the smallest category, custom application, 2024 was an off year. Overall, according to the survey data, revenues in this category dropped $500 million, from $2.8 billion in 2023 to $2.3 billion this year. Market share for this category also was down, off 1% from 6% in 2023 to 5%.

However, for custom application, virtually all of this revenue decline stemmed from the fact that the category includes ag technology products within its overall numbers. These were off significantly from 2023 due to a variety of factors.

But the biggest loser in terms of revenues/market share was the largest category, fertilizer. Not too many years ago, the fertilizer category represented more than half of all crop inputs/services (51%, to be exact) sold for CropLife 100 ag retailers on an annual basis. For the past few years, however, sales for this category have steadily dropped.

In 2024, this decline accelerated quite a bit. According to the 2024 CropLife 100 survey, the fertilizer category had sales of $19.9 billion this year, down $2.5 billion from the 2023 total of $22.4 billion. As a result of this loss, market share for the category fell even further back, down from 48% in 2023 to 46% this year. This is essentially the same market share the fertilizer category held back at the start of the 2020s.

The Smaller, the Better

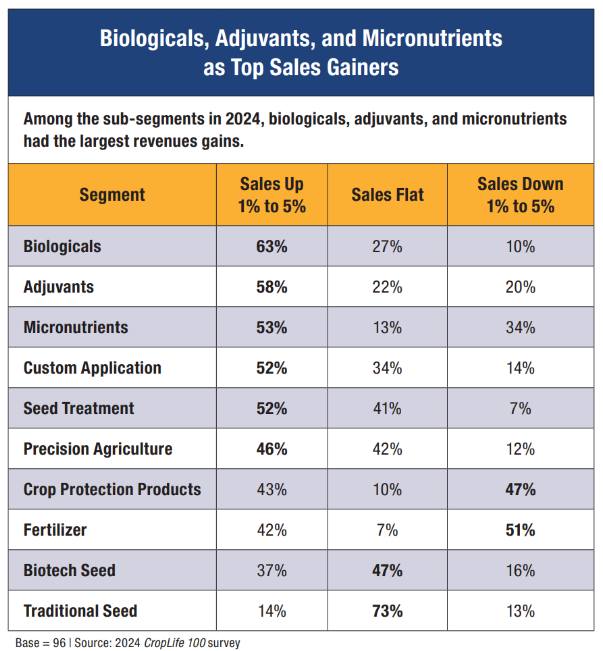

Even with all these poor numbers, the 2024 CropLife 100 survey of the nation’s top ag retailers did provide some positive news. Indeed, for this year’s growing season, it seems that the smaller the segment, the better it performed.

Each year, CropLife tracks the sales performances of 10 different sub-segments of the ag retail business. On the survey, we asked respondents to tell us if their sales for each of these sub-segments have grown, declined, or stay flat year-over-year. And in 2024, three of the smaller segments lead the industry in overall growth.

Each year, CropLife tracks the sales performances of 10 different sub-segments of the ag retail business. On the survey, we asked respondents to tell us if their sales for each of these sub-segments have grown, declined, or stay flat year-over-year. And in 2024, three of the smaller segments lead the industry in overall growth.

Coming in best for the 2024 growing season was biologicals. According to the nation’s top ag retailers, 63% saw their revenues in this segment improve by between 1% and more than 5% for the year. Another 27% had flat biologicals sales, with 10% recording sales declines.

Two other sub-segments that performed well in 2024 were adjuvants and micronutrients. For these sub-segments, 58% and 53% of CropLife 100 members, respectively, recorded revenue gains of between 1% and more than 5%. The other two sub-segments to see more than half of respondents increase their revenues were custom application and seed treatments (both at 52%).

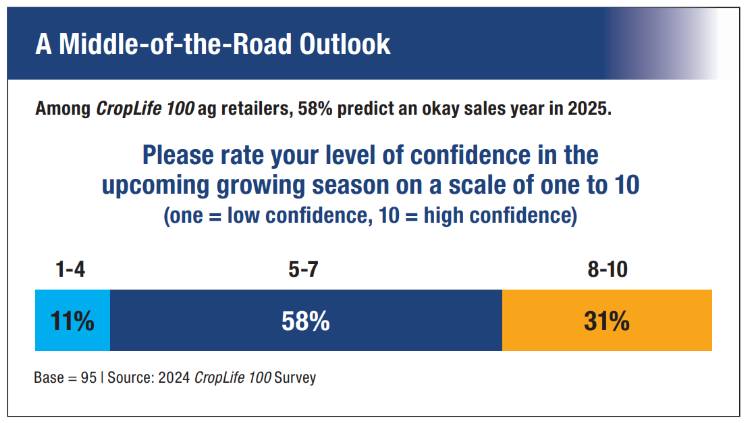

Given all the negative numbers floating around from the 2024 CropLife 100 survey, the nation’s top ag retailers say that their grower-customers are still expecting the 2025 growing season to be a bit better in terms of overall performance. In the survey, CropLife asks respondents to tell us how their grower-customers would rate the prospects for the upcoming year on a scale of one to 10 — one being extremely bad to 10 being extremely good, with varying degrees of bad and good mixed in-between.

Given all the negative numbers floating around from the 2024 CropLife 100 survey, the nation’s top ag retailers say that their grower-customers are still expecting the 2025 growing season to be a bit better in terms of overall performance. In the survey, CropLife asks respondents to tell us how their grower-customers would rate the prospects for the upcoming year on a scale of one to 10 — one being extremely bad to 10 being extremely good, with varying degrees of bad and good mixed in-between.

According to the 2024 CropLife 100 survey, 11% of the nation’s top ag retailers say their grower-customers are preparing for a rough economic season next year, rating the year between a one and a four. However, the other 89% foresee more positive results for 2025.

Based upon the survey data, the vast majority of CropLife 100 ag retail grower-customers believe the 2025 growing season will rate between a five and a seven on the 10-point scale — pretty positive given how things played out during 2024. Better still, 31% of respondents say their grower-customers believe the 2025 growing season will rate between an eight and 10 in terms of profitability.

This would seem to bode well for the agricultural marketplace come next year. As always, time will tell.

Subscribe Today For