2016 Fertilizer Report: Another Really Rough Year For Ag Retail

December 7, 2016

December 7, 2016

As the 2016 planting season got underway, ag retailers were hopeful that a relatively normal weather year would re-energize fertilizer demand among grower-customers.

In many ways, the fertilizer category cannot seem to catch a break. During the early part of the 2010s decade, as commodity prices hit all-time record highs, grower-customers were applying fertilizer to their crop fields with reckless abandon. By the time the 2012 CropLife 100 data was compiled, fertilizer revenues for the nation’s top ag retailers were above the $15 billion mark, holding down a 55% market share compared with all other crop inputs/services. At this point, it seemed to many market watchers that the sky was the limit and fertilizer would easily top a 60% market share figure within a few short years.

Yet, as 2014 rolled around, there were signs that this market dominance might not materialize after all. During that year, as commodity prices began to drop, fertilizer demand waned as well. By the end of the year, the fertilizer category’s sales had dropped to $14.8 billion, with the market share back down below 50%. An extremely wet spring season during 2015 further cramped fertilizer category sales, with the sector falling back another $300 million for the year to $14.5 billion.

As the 2016 planting season got underway, ag retailers were hopeful that a relatively normal weather year would re-energize fertilizer demand among grower-customers, particularly since many of them had “mined” their soils for a few seasons to keep their overall costs down.

But this apparently didn’t happen. When the final numbers were tallied from the 2016 CropLife 100 ag retailers survey, the fertilizer category has once again taken a serious revenue/market share hit. For the year, revenues stood at $13.5 billion, down $1 billion from 2015. This 7.4% decline in sales also places fertilizer’s market share among crop inputs/services for CropLife 100 ag retailers at 45% — virtually the same percentage the category held back in the early years of the 21st century.

A Surprising Outcome

Given what market analysts were hearing earlier in 2016, this steep drop in fertilizer revenues for CropLife 100 ag retailers probably comes as something of a surprise. Back in the summer, Andy Jung, Director of Market and Strategic Analysis for The Mosaic Co., told CropLife® magazine that the anticipated drop-offs in crop nutrients demand for the fall weren’t looking likely. “Frankly, we heard talk about expected application curtailments last fall when grain prices were pretty much in line with where they are today,” said Jung. “Those cutbacks never really transpired.”

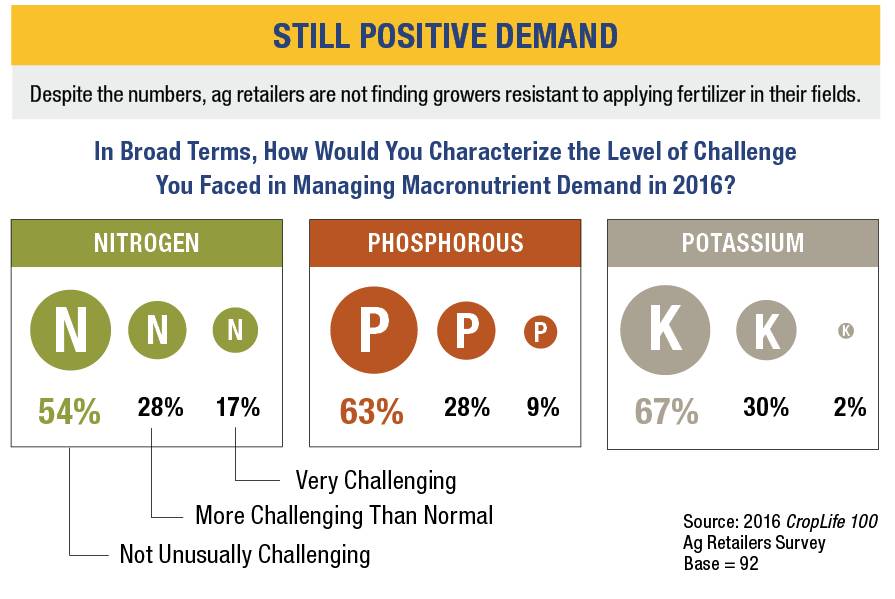

CropLife 100 ag retailers also noted this as well. During the 2015 CropLife 100 survey, respondents were asked to describe the level of challenge faced by them during the calendar year to spurring fertilizer demand amongst their grower-customers. The majority (more than 50% collectively) indicated that this effort on their part was “not unusually challenging,” when it came to convincing customers to apply the various forms of macronutrients in their crop fields.

And these percentages were even stronger for the 2016 survey. According to CropLife 100 ag retailers, 54% found convincing their grower-customers to use nitrogen in their fields “not unusually challenging.” The numbers were even better for phosphorus and potassium, coming in at 63% and 67%, respectively. Only 9% of respondents found convincing growers to use phosphorus in 2016 “very challenging,” with 2% describing this situation existed when it came to potassium application. Only nitrogen usage proved somewhat difficult to promote, with 17% of respondents saying this was “very challenging” in 2016.

Now that the fertilizer category has experienced four straight years of declining revenues, will 2017 mark a fifth? Obviously, the jury is still out on this matter, but looking at some of the expected crop mix numbers doesn’t seem to bode well for the category.

The Outlook for 2017

Primarily, corn is the most fertilizer intensive crop in the market. However, with corn commodity prices currently resting in the $3 per bushel range and the 2016 looking strong in many parts of the country, ag retailers are anticipating many of their grower-customers to look to plant other crops come the 2017 growing season. According to the survey, 43% of respondents believe corn acreage in their areas will be down 1% to 10% in 2017. Only 25% expect the amount of corn to increase.

Expected to pick up the slack will be soybeans, which are currently selling for a much stronger $9-plus per bushel on the commodity market. Overall, 53% of survey respondents believe soybean acreage will grow between 1% and 10% during 2017. Only 17% expect to see the soybean acreage in their regions drop for the year.

Subscribe Today For