Buying Intentions Survey: Why 2026 Looks Like 2025 for Ag Retailers

![]() If ag retailers and their grower-customers enjoyed the way the agricultural marketplace performed in 2025, then they are in for a treat. In terms of product purchases, the upcoming 2026 growing season looks to be a mirror image of the previous year in each and every category. However, in each sector, there will be at least one segment that is projected to see higher sales than during the 2025 growing season.

If ag retailers and their grower-customers enjoyed the way the agricultural marketplace performed in 2025, then they are in for a treat. In terms of product purchases, the upcoming 2026 growing season looks to be a mirror image of the previous year in each and every category. However, in each sector, there will be at least one segment that is projected to see higher sales than during the 2025 growing season.

This was the overall finding of the 12th annual CropLife® Magazine Buying Intentions Survey. Each year for more than a decade now, CropLife has asked ag retailers to tell us about the expected buying habits of their grower-customers for the upcoming year based upon their market insights and customer feedback. Sales-wise, 2026 is projected to play out much as 2025 did. Still, a few product segments can expect to see increased revenue interest.

So, without further ado, let’s drive into the numbers.

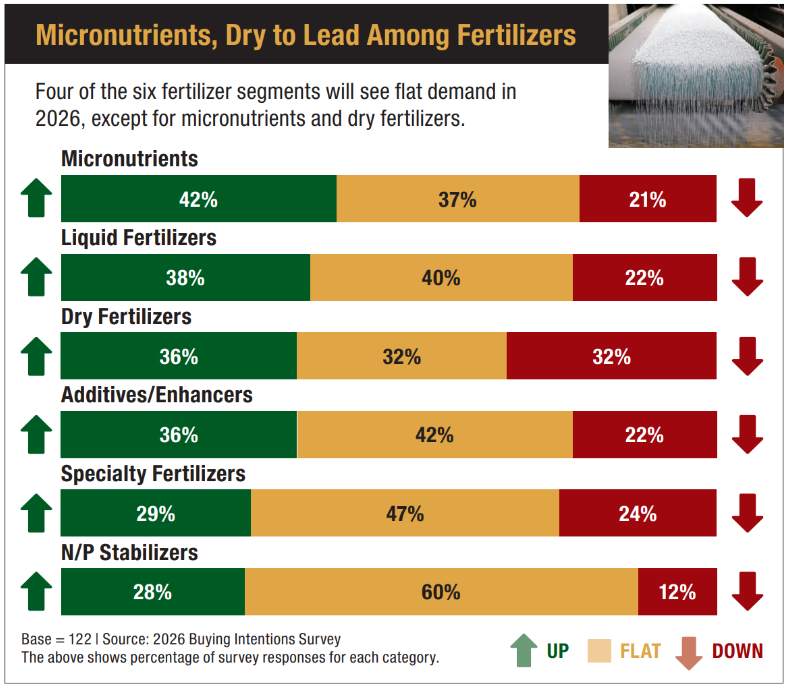

The Fertilizer Outlook

As the largest category among crop inputs for ag retailers, the fertilizer sector has been on a rollercoaster ride the past two years. Higher-than-normal prices and global supply chain issues (particularly the threat of tariffs) have weighed heavily upon the overall market’s performance. Despite these facts, the fertilizer category did manage to recover from its dismal 2024 market results, when revenues dropped $2.5 billion to $19.9 billion. In 2025, the sector’s revenues again hit $19.9 billion, showing signs that at least some of the market volatility that plagued the category during 2023 and 2024 was finally beginning to stabilize.

Still, heading into 2026, ag retailers surveyed by CropLife don’t expect much product segment growth to occur. In fact, of the six segments tracked in the Buying Intentions Survey, respondents predict four of them — liquid fertilizers, specialty fertilizers, nitrogen/phosphorus (N/P) stabilizers, and additives/enhancers — will see flat sales volumes among ag retailers during the upcoming growing season. This “level of flatness” ranges from a low of 40% for liquid fertilizers to a high of 60% for N/P stabilizers.

However, two fertilizer segments can expect higher sales volumes during the 2026 growing season. Leading the way will be micronutrients. According to the survey data, 42% of respondents expect their purchases of these products to increase by between 1% and more than 11% this year. Thirty-seven percent are planning for flat micronutrient spending, while the remaining 21% expect to decrease purchases in this segment by between 1% and more than 11%.

For dry fertilizers, the buying pattern for 2026 will be similar to that of micronutrients. According to the survey data, 38% of respondents predict that their spending in this segment will grow by between 1% and more than 11%. The other 64% are evenly split — 32% expect flat spending in dry fertilizers while 32% plan to decrease spending in this area by between 1% and more than 11%.

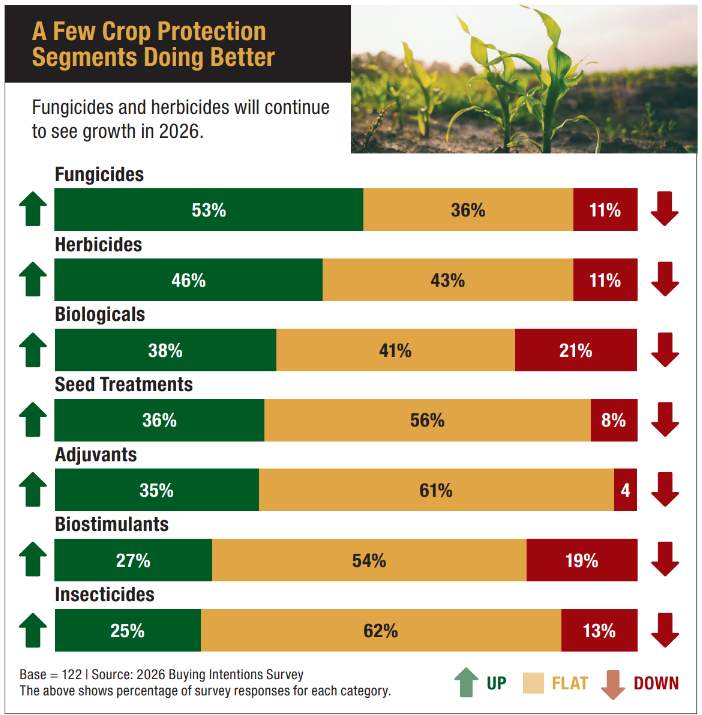

The Crop Protection Products Outlook

In many ways, the crop protection products category followed a similar path to that of fertilizer during 2025. According to data from the 2025 CropLife 100 survey, overall revenues for this sector last year topped $15.3 billion — the identical mark crop protection products managed to record during the 2024 growing season.

Given this result, it should also surprise no one reading this report that the 2026 buying intentions of ag retailers and their grower-customers look very similar to those reported in the 2025 Buying Intentions Survey. Two of the seven segments tracked in the survey for this category are expected to show sales improvement. The other five segments are projected to remain flat.

Expected to perform best this year is the fungicides segment. As crop diseases such as tar spot and crown rot have expanded their geographic reach over the past few years, the demand for crop protection products that can help control these pathogens has steadily increased. So, according to the 2026 Buying Intentions Survey results, 53% of respondents predict that their fungicides spending will increase by between 1% and more than 11% for the 2026 growing season. Another 36% expect flat fungicide spending this year, with the remaining 11% expecting to see spending decline for fungicides.

It’s a similar story for herbicides. In recent years, weed researchers have continued to discover new species resistant to commonly used herbicide active ingredients, with Palmer amaranth and waterhemp becoming particularly hard to control.

So, according to survey respondents, 46% of ag retailers are anticipating increased herbicide spending for their operations during 2026, with increases by between 1% and more than 11%. A similar percentage — 43% — predict their herbicide segment spending this year will remain flat. The remaining 11% think their herbicide spending for the 2026 growing season will decline by between 1% and more than 11%.

As for the other five segments in the crop protection products category — biologicals, biostimulants, adjuvants, seed treatments, and insecticides — spending in 2026 is expected to be on par with 2025 according to most of the 2026 Buying Intentions Survey respondents. This “flatness” ranges from a low of 41% for biologicals to a high of 62% for insecticides.

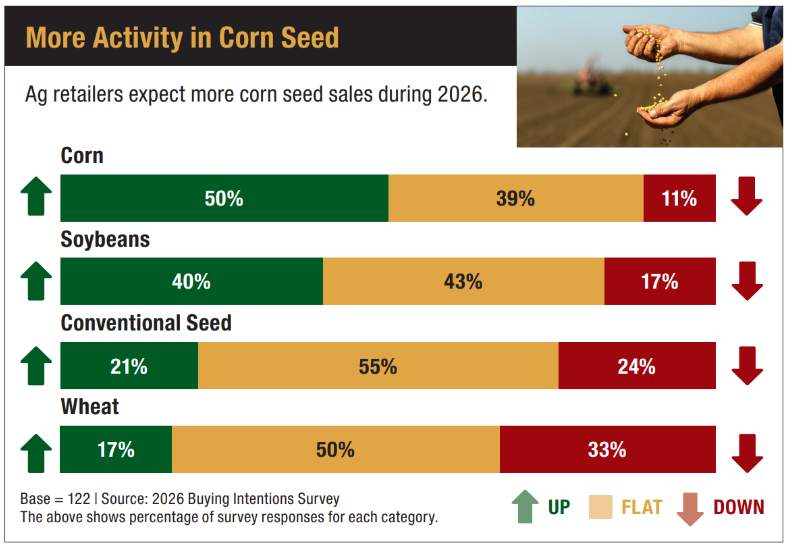

The Seed Outlook

For several years now, the seed category has remained relatively flat among ag retailers compared with other crop inputs, and this pattern continued to play out during the most recent calendar year. According to the 2025 CropLife 100 survey of the nation’s top ag retailers, overall seed sales last year were $5.7 billion — down only slightly from the 2024 figure of $5.8 billion.

Given these facts, perhaps it should come as no surprise that 2026 Buying Intentions Survey respondents expect the majority of the seed spending to remain flat during the 2026 growing season as well. This is true for three of the seed segments tracked in the survey — soybeans, wheat, and conventional seeds. Forty-three percent of respondents predict their soybean seed spending will be identical to that in 2025. Fifty percent say their wheat seed spending will be flat for 2026, and 55% of respondents expect their conventional seed spending to remain the same as in 2025.

However, there is one seed segment where 2026 Buying Intentions Survey respondents do expect to see increased activity — corn. According to early USDA planting intentions results from fall 2025, U.S. growers are expected to plant between 93 million and 95 million acres of corn this year.

Perhaps motivated by this news, 50% of respondents to the 2026 Buying Intentions Survey expect that their corn seed spending will improve during the upcoming growing season by between 1% and more than 11%. Another 39% of respondents expect flat corn seed spending for the year. The remaining 11% think that their corn seed spending will fall by between 1% and more than 11%.

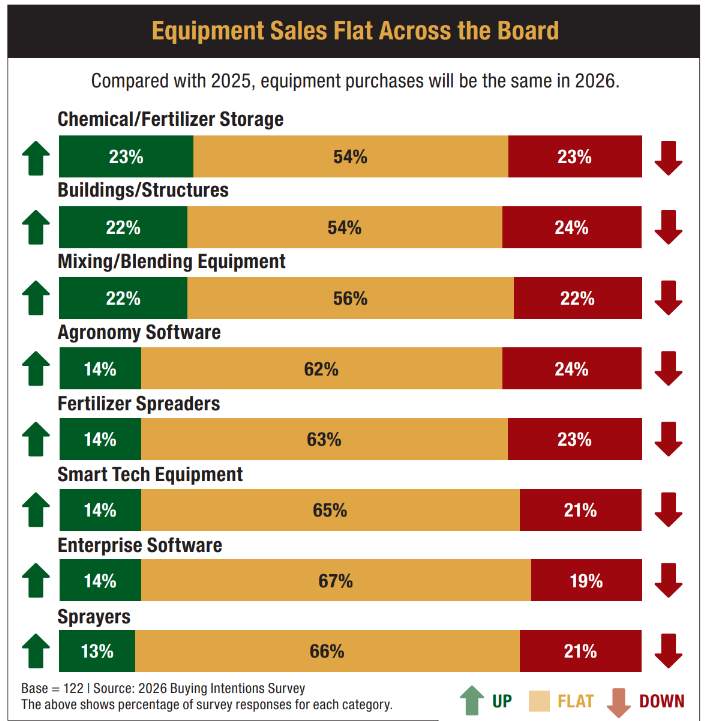

The Equipment Outlook

As has been the case the past few years of the annual Buying Intentions Survey, ag retailers predict overall sameness in their spending for products that fall into the equipment category. In fact, only three segments can expect spending increases from more than 20% of ag retailers.

Based upon the data, it seems as if the most activity in spending for 2026 among the equipment segments will be in facility building. The top two segments expected to see spending growth this year are chemical/fertilizer storage at 23% and buildings/structures at 22%. The only other segment in this range is mixing/blending equipment at 22%.

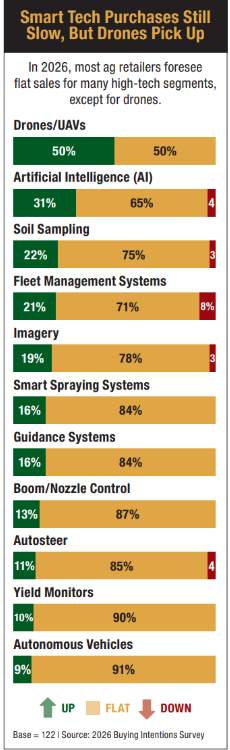

The Smart Tech Outlook

Like virtually every other category, 2026 Buying Intentions Survey respondents believe the Smart Tech sector will see overall flat spending during the upcoming growing season. However, this is one notable exception on this list.

For several years now, the use of drones for scouting and application work in crop fields has been on the rise (no pun intended). At numerous trade shows and industry events throughout 2024 and 2025, many educational sessions dealt with drones use and regulations for operating them. And perhaps this interest in drones will reflect in increased purchasing decisions when it comes to this segment in 2026 as well, at least based upon the data.

For several years now, the use of drones for scouting and application work in crop fields has been on the rise (no pun intended). At numerous trade shows and industry events throughout 2024 and 2025, many educational sessions dealt with drones use and regulations for operating them. And perhaps this interest in drones will reflect in increased purchasing decisions when it comes to this segment in 2026 as well, at least based upon the data.

According to the 2026 Buying Intentions Survey, half of the respondents (50%) expect to increase their spending on drones by between 1% and more than 11% this year. That’s double the mark the drones segment saw in the 2025 Buying Intentions Survey, when only one-quarter of respondents (25%) planned to up their spending in this area.

If there’s another positive to take away for the Smart Tech category in 2026, it’s the lack of planned spending declines. According to the 2026 Buying Intentions Survey, there are six Smart Tech segments that had no respondents say they plan to decrease their investment in these products during the upcoming growing season.

About The Survey

The 12th annual CropLife Buying Intentions survey was sent to readers in November and early December 2025. In total, there were 122 surveys returned with valid answers.

In terms of breakout, 67% of the respondents identified themselves as being ag retailers/cooperatives. Another 6% said that their companies were classified as fertilizer producers. Eight percent indicated they were pesticide manufacturers or formulators. Another 8% identified as manufacturers of equipment or components. The remaining 11% identified themselves as “others.”

CropLife would like to thank everyone that took part in this year’s survey. Your insights are appreciated!

Subscribe Today For