Fertilizer Market Held Steady in 2025, But Signs of Strain Emerged

Considering how much “negative” market buzz there was during the 2025 growing season, the fertilizer category performed remarkably well. Still, there were hints that trouble could be just around the corner.

According to data collected in the 2025 CropLife 100 survey, the fertilizer category saw its overall revenues remain relatively flat for the year. Sales for 2025 came in at $19.9 billion – the identical sales figure that the category recorded during the 2024 growing season. Furthermore, the category was able to hold onto its overall market share among the nation’s top ag retailers vs. all the other crop inputs/services categories at 46%.

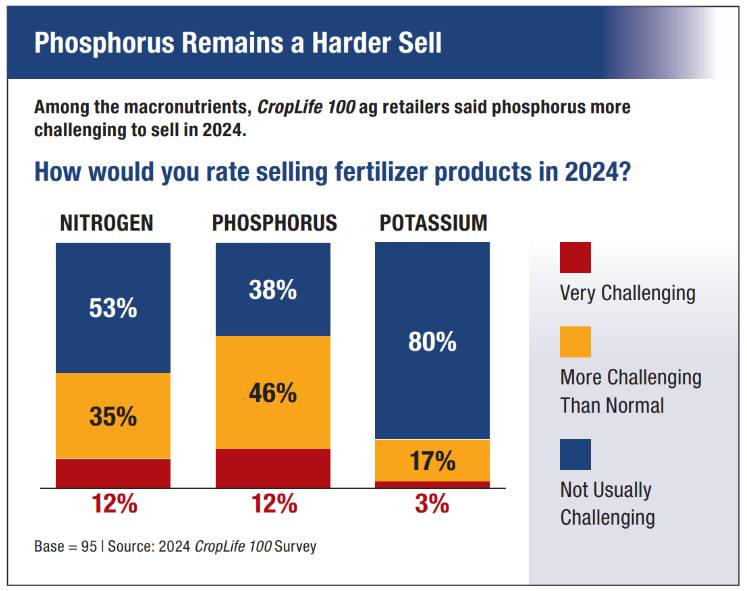

Despite these numbers, many CropLife 100 ag retailers told CropLife® Magazine that convincing their grower-customers to apply certain macronutrients was a much more difficult task than it has been in recent growing seasons.

In particular, respondents said, phosphorus application was a really tough sell in 2025. According to the 2025 CropLife 100 survey data, 30% of the nation’s top ag retailers described convincing their grower-customers to apply phosphorus as “very challenging.” This represented a big jump in percentages compared with the 2024 CropLife 100 survey, where only 16% of respondents said phosphorus sales were “very challenging.”

In addition, 35% of 2025 CropLife 100 ag retailers described convincing their grower-customers to apply phosphorus as “more challenging than normal.” The remaining 35% of respondents said phosphorus sales for them were “not usually challenging” compared with prior growing seasons.

Even the most popular macronutrient in terms of usage – nitrogen – wasn’t immune to this application resistance from grower-customers. In the 2024 CropLife 100 survey, 12% of respondents said convincing their grower-customers to apply nitrogen-based fertilizer was “very challenging.” In 2025, this percentage increased to 16%. Another 45% of the nation’s top ag retailers said getting their grower-customers to apply nitrogen to their fields was “more challenging than normal” – up from 35% in the 2024 CropLife 100 survey data. Only 39% of CropLife 100 ag retailers described their efforts to get customers to apply nitrogen fertilizers as “not usually challenging.”

The only macronutrient that continued to meet with “universal approval for application among grower-customers” in 2025 was potassium/potash. According to the 2025 CropLife 100 survey, 70% of respondents said convincing their grower-customers to purchase potassium was “not usually challenging.” Twenty percent said potassium sales in 2025 were “more challenging than normal.” The remaining 10% found making potassium sales to their grower-customers “more challenging than normal” for the 2025 growing season.

More Corn Expected

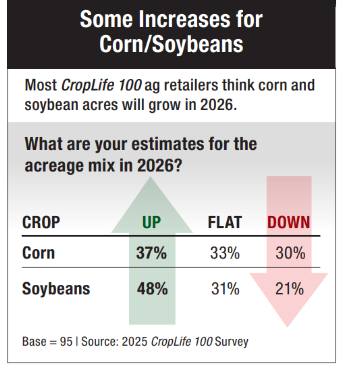

With the 2025 fertilizer numbers in the books for CropLife 100 ag retailers, the question now turns to how will the 2026 growing season play out? According to many market watchers, the lack of export sales on the soybean front for 2025 could push many growers to decide to plant more corn acres during the 2026 growing season. And by their nature, corn plants are much more dependent upon crop nutrition products than their soybean counterparts.

But do CropLife 100 ag retailers think this will happen? The data suggests a different scenario might play out instead.

But do CropLife 100 ag retailers think this will happen? The data suggests a different scenario might play out instead.

In terms of acreage numbers for next year, a slight majority – 37% – of CropLife 100 ag retailers expect corn acreage for 2026 to increase between 1% and more than 10% for their grower-customers. Another 33% of respondents believe corn acreage in 2026 will be identical to what it was in 2025 (just over 97 million acres). The remaining 30% believe corn acreage next year will drop between 1% and more than 10%.

For soybeans, the outlook for 2026 is even brighter. Despite the trade issues in 2025, 48% of 2025 CropLife 100 ag retailers predict soybean acreage among their grower-customers will increase between 1% and more than 10%. Thirty-one percent predict flat acreage for soybeans in 2025 (just over 83 million acres). The remaining 21% believe soybean acreage in their areas will fall between 1% and more than 10%.

Subscribe Today For