Analysts to Growers: At Least One More Year of Belt-Tightening

January 31, 2018

January 31, 2018 Hoping to get a read on growers’ appetite for spending this coming season? The smart money is they’ll be doing more belt-tightening this year – and probably for a few more years after that.

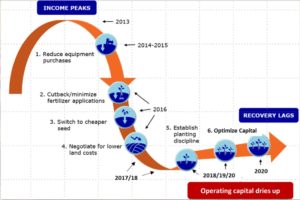

The cycle of the current ag economy hit its peak in 2013 and now, after multiple seasons of declining crop prices and farmer belt-tightening, is expected to remain largely flat until 2020. Source: Rabobank AgriFinance | Farm Credit Mid-America

“Use careful financial management” was the core advice given to hundreds of producers at the DTN/Progressive Farmer Ag Summit held in Chicago, IL, in early December. And while the world could change before the first seed hits the ground this spring, directionally the message resonates with what generally is assumed to be true: A recovery in the ag economy since 2013 continues to lag (see graph).

Farmers have ratcheted down their production costs over the past several years, but they still remain above farm-gate prices, according to Steve Allard, Chief Credit Officer and Senior Vice President of Farm Credit Mid-America; and Curt Hudnutt, Executive Vice President and Head of Rural Banking North American at Rabo AgriFinance.

The good news? We are not moving into a 1980s-farm-crisis scenario. The environment is different today, not least because interest rates are fixed now rather than variable as they were then. The not-so-good news? With an increase in 2017 stocks, prices are projected to remain low longer-term, with a baseline average received price of $3.50-$3.80 per bushel for corn and $9.25-$9.80 per bushel for soybeans.

This means tight margins over the long term.

How Growers Will React

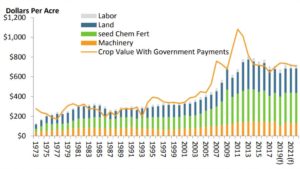

Even amid generally rising farm expenses across the board, machinery hit a high in 2011 but has tapered off since, and is expected to remain mostly flat into the next decade. Source: Rabobank AgriFinance | Farm Credit Mid-America

Farmers were advised not to relent in their hawkish attention to their financial profiles, with particular attention paid to the big areas where their hard-earned dollars go right back out the farm gate along with their crops. These expenses had a particular run-up in dollars per acre from about the mid-2000s until the bottom started to drop out on commodity prices in 2013 (see graph).

Crop inputs. Seed, crop protection, and fertilizer together account for 40%-42% of total crop value – a range that is not likely to budge much even through the current round of mergers among the multinational crop protection companies. Advice from Allard and Hudnut: “Negotiate.”

Machinery. The price spent per acre on machinery really spiked in 2011 – more than likely a lot of it in precision equipment including autosteer. Why? Because farmers were making a lot of money. Now equipment expenditures hover at about 15%-18% of expected crop value and are forecast to remain relatively flat as measured by dollars per acre until at least 2021.

Land. With a generally flattening or downward adjustment in land values over the last several years, Allard, Hudnut, and others at the conference pressed hard on producers to intensify negotiations on land leases. For growers to ride out the next several years, they’ll need to lean out the price of land from its current average of 40% of total crop value down to 35% or even 30%. To do this they’ll likely need to negotiate with existing landholders, they said, because a lot of farmable land still is held by widows and retired farmers.

New farming strategies. Allard and Hudnut advised growers to break out of long-established patterns – for instance through group-buying, economies of scale, data management and analysis, peer and industry benchmarking, and carrying out defined and disciplined marketing plans. They also encouraged them to “put your bias aside” regarding all-natural and organic crops and “do what’s right for your operation.”

The next two years will be pivotal, Allard and Hudnut said. If all goes as expected, the “highest probability” for breakeven on corn and soybean farms comes sometime after the 2018 season – if farmers exercise discipline in planted acres and lending/borrowing, and if export growth of crop commodities and animal protein remains interrupted.

In the meantime, if your customers lean on you for both better pricing and a continuing level of advice and service in the year ahead, you’ll likely be counted among a majority of service providers.

Subscribe Today For